HDFC Life

CMP: ₹584.45

Recommendation: Buy

Investment Horizon: 3 years

Veer Trivedi – Research Analyst

Date – December 01, 2022.

Outlook and view

Life Insurance is a high growth business which is fairly underpenetrated and has a high protection gap. The top four player constitute around 85% of the New Business premium (NBP) of the industry. Thus, as the sector will grow the big players involved are bound to grow too. HDFC Life is one of the major players in this segment. To win at this industry there are essentially two major criteria which are required. A diversified product mix with a focus on protection business and a strong distribution channel backed by a strong bank. HDFC Life fulfills both the criteria effectively. A strong product mix, solid cost efficiency measures and the support from the regulator will ensure a good performance going forward. The stock has witnessed underperformance in recent period. This correction had made the stock available at an attractive price.

Key Positives

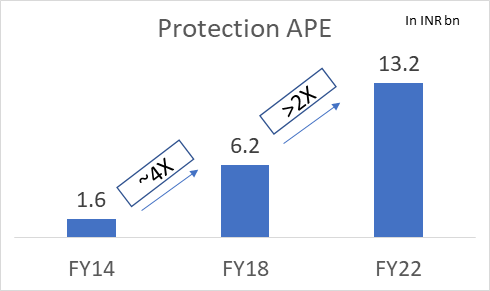

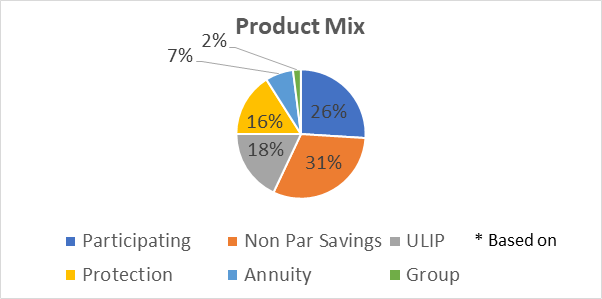

Diversified product Mix: HDFC Life has a balanced product mix versus peers. Non-par savings has a share of 31% to its total APE, whereas the Participating share stands at 26% and protection at a healthy 16%. HDFC life had a first mover advantage in the protection business and thus have been able to generate a good market share in this segment.

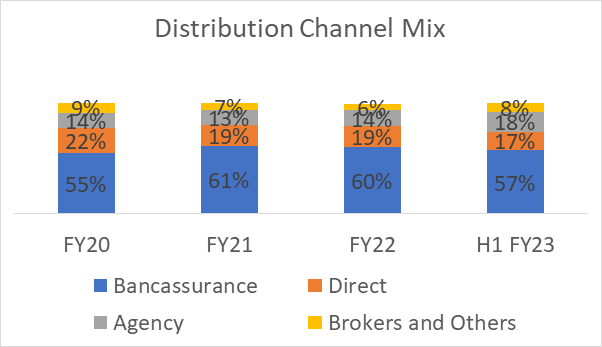

Strong distribution network: The company has a well-diversified distribution network. The key to winning the market share in Life Insurance is to have a strong Bancassurance presence. Over the years the share of Bancassurance in HDFC Life has grown at a good rate. In FY18 the Banks formed a 47% share in its distribution mix vs 55% in FY22.

Exide merger complimentary for HDFC Life: The acquisition will add 35% to the company’s existing agent base. Further, Exide Life has a significant presence in tier 2-3 cities and down south. This will aid the company to push the growth peddle.

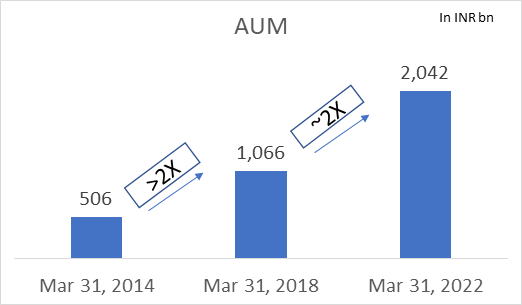

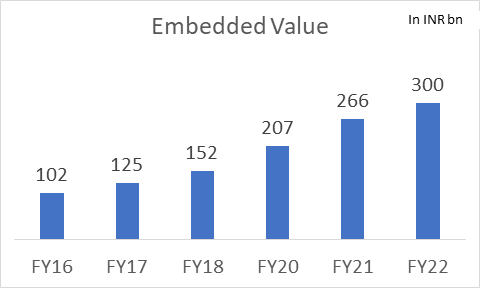

Other metrics robust: In the latest quarter the company generated a strong Return on EV at 19%. The Life Insurer’s persistency ratio stood at 87.1% which improved 120 bps year-on-year. The company’s AUM grew by 17.6% YoY, whereas the total APE witnessed growth of 18.1% YoY.

Key Risks

Stress in HDFC Bank distribution: The growth in the HDFC Bank channel which contributes around 48% of its premium has slowed down. However, post the merger of HDFC Ltd and HDFC Bank, HDFC Life will become the subsidiary of the HDFC Bank and thus there would be alignment with the goals of HDFC Bank and HDFC Life.

Subdued Premium Growth: In the current half year period i.e., H1 FY23 HDFC Life has grown at a slower pace than its peers. The company has also witnessed weakness in its Individual protection segment.

About the company

HDFC Life is a leading Life Insurance provider in India. The company offers Individual and group products for the savings and protection requirements of the customers. The company as of H1 FY23 has a total AUM of INR 2,249 billion. HDFC Life is a joint venture between HDFC Ltd and Standard Life Aberdeen. HDFC Life has a wide distribution network which comprises of individual agents, bancassurance partners, third-party agents etc.

Financials Snapshot

| Particulars | H1 FY23 (Pre-Merger) | H1FY22 | Growth | FY22 | FY21 | H1 FY23 (Post-Merger) |

| New Business Premium (Indl. + Group) | 109.2 | 103.6 | 5% | 241.5 | 201.1 | 113.2 |

| Renewal Premium (Indl. +Group) | 108.0 | 89.2 | 21% | 218.1 | 184.8 | 120.1 |

| Total Premium | 217.2 | 192.9 | 13% | 459.6 | 385.8 | 231.9 |

| Individual APE | 37.9 | 34.3 | 11% | 81.7 | 71.2 | 41.1 |

| Overall APE | 45.5 | 41.1 | 11% | 97.6 | 83.7 | 49.1 |

| Profit after Tax | 6.8 | 5.8 | 18% | 12.1 | 13.6 | 6.9 |

| Assets Under Management | 2,043.9 | 1,912.1 | 7% | 2,041.7 | 1,738.4 | 2249.1 |

| Indian Embedded Value | 330.2 | 287.0 | 15% | 300.5 | 266.2 | 360.2 |

Key Metrics:

| Particulars | H1 FY23 (Pre-Merger) | H1FY22 | FY22 | FY21 | H1 FY23 (Post-Merger) |

| Overall New Business Margins | 27.6% | 26.4% | 27.4% | 26.1% | 26.2% |

| Operating Return on EV | 17.7% | 16.1% | 16.6% | 18.5% | NA |

| Operating Expenses / Total Premium | 14.3% | 12.0% | 12.3% | 12.0% | 14.7% |

| Total Expenses (OpEx + Commission) / Total Premium | 18.5% | 16.3% | 16.5% | 16.4% | 19.3% |

| Return on Equity | NA | 13.5% | 10.1% | 17.6% | 12.4% |

| Solvency Ratio | 210% | 190% | 176% | 201% | 210% |

| Persistency (13M / 61M) | 88%/54% | 86%/52% | 87%/54% | 85%/49% | 87%/51% |

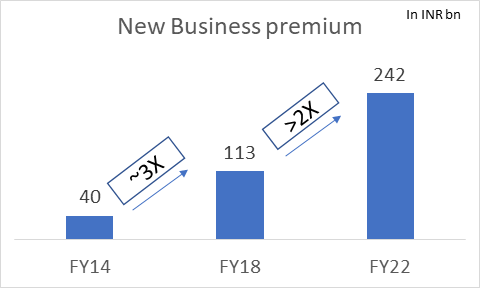

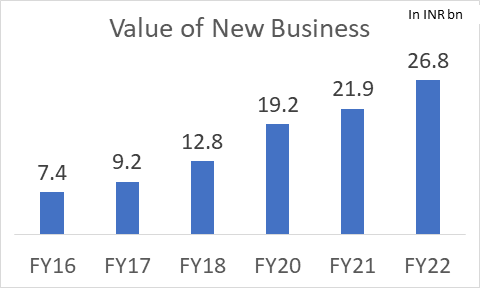

Story In charts:

Easy & quick

Easy & quick

Leave A Comment?