Can you picture a country without a banking system? Banks are the backbone of every economy. If they collapse, the entire country eventually collapses. Every citizen places a great amount of trust in this system. Individuals and companies turn to banks for their funding needs. A nation's ability to assemble its capital effectively depends on them. This is why banks flourish amidst all political, economic, and natural crises. This makes the banking sector one of the most attractive sectors for investment. However, with great power comes great risks and responsibilities. You must not invest in a bank just because your friend says it is a good idea. Or because a news channel forecasted a profitable investment for a particular bank. Always conduct your own research before buying a banking stock.  If you think that analysing a sector or a company is something only an analyst can do, then you are wrong. By the end of this article, you will be able to conduct your own independent research on banking stocks. We will understand the ins and out, from understanding how banks earn money to how can they generate returns for us. Investing in banks requires a careful analysis of financial data. Checking few general ratios is not enough. Hence, we will focus on the elements used specifically to analyse the efficiency of banks. All you need to do is patiently keep reading till the end. Our aim is to show you how you can analyse banking stocks. Let me tell you, this is going to be in an absolutely simple and easy-to-understand language. In this article, you will learn what is Capital Adequacy Ratio, CASA, Slippage, Gross & Net NPA, and PCR. Understand the relation between NII, NIM, and NPA. And many more qualitative analysis parameters. I can promise that after reading this article you would be able to analyse any bank of your choice. So, let’s begin!

If you think that analysing a sector or a company is something only an analyst can do, then you are wrong. By the end of this article, you will be able to conduct your own independent research on banking stocks. We will understand the ins and out, from understanding how banks earn money to how can they generate returns for us. Investing in banks requires a careful analysis of financial data. Checking few general ratios is not enough. Hence, we will focus on the elements used specifically to analyse the efficiency of banks. All you need to do is patiently keep reading till the end. Our aim is to show you how you can analyse banking stocks. Let me tell you, this is going to be in an absolutely simple and easy-to-understand language. In this article, you will learn what is Capital Adequacy Ratio, CASA, Slippage, Gross & Net NPA, and PCR. Understand the relation between NII, NIM, and NPA. And many more qualitative analysis parameters. I can promise that after reading this article you would be able to analyse any bank of your choice. So, let’s begin!

Types of Banks in India:

There are more than 97,605 banks in India. But only 35 banks are listed on National Stock Exchange which are either private banks, public banks, or small finance banks. If you want to discover lucrative opportunities among them then you must first understand how the sector works.  Public Sector Banks Government has more than 50% stake in these banks. Top public sector banks include State Bank of India (SBI), Bank of Baroda (BOB), Indian Bank, etc. You can check various Public Sector Banks here. Private Sector Banks These banks are owned by a private owner. For example, HDFC Bank, ICICI Bank, etc. However, they are regulated by the RBI to protect the public interest. You can check various Private Sector Banks here. Small Finance Banks These banks provide basic banking services of acceptance of deposits and lending. Their aim is to provide financial service to sections of the economy not being served by other banks. For example, marginal farmers, small business units, unorganised sector entities, etc. All these banks collectively keep the economy running. Banking operations are unlike any other sector which uses commodities to produce goods. Money is the only raw material for banks. Let’s have a quick look and understand how money works for banks.

Public Sector Banks Government has more than 50% stake in these banks. Top public sector banks include State Bank of India (SBI), Bank of Baroda (BOB), Indian Bank, etc. You can check various Public Sector Banks here. Private Sector Banks These banks are owned by a private owner. For example, HDFC Bank, ICICI Bank, etc. However, they are regulated by the RBI to protect the public interest. You can check various Private Sector Banks here. Small Finance Banks These banks provide basic banking services of acceptance of deposits and lending. Their aim is to provide financial service to sections of the economy not being served by other banks. For example, marginal farmers, small business units, unorganised sector entities, etc. All these banks collectively keep the economy running. Banking operations are unlike any other sector which uses commodities to produce goods. Money is the only raw material for banks. Let’s have a quick look and understand how money works for banks.

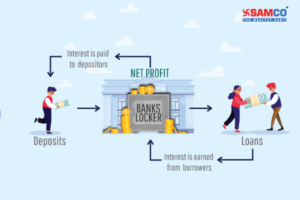

Banking Model - How Does a Bank Work?

The primary business of a bank is to accept deposits and give out loans. The loans given by the banks are their asset on which they earn interest. On the other hand, deposits that banks accept are their liabilities. They have to pay interest to depositors on their deposits. Thus, earned interest minus paid interest is their profit. This is their bread and butter.  To check the bank’s interest income, we must check their income statement.

To check the bank’s interest income, we must check their income statement.

a. Interest Income

Banks earn interest on the loans they have issued. This is their main source of income. In other words, this is their lifeline.

HDFC Bank Annual Report: Profit and Loss Account (2019-20)

For example, we can see that about 83% of HDFC Bank’s total income is interest earned. This amount comprises of –

- Interest earned from issued loans

- Interest earned from investments

- Interest earned on balances with Reserve Bank of India (RBI) and other inter-bank funds

Interest earned on advances and investments are self-explanatory. Banks invest in various government risk-free securities and earn interest from these investments. This forms a part of their primary interest income. But how do banks earn interest from RBI? Banks have to reserve a certain portion of the amount deposited by customers with RBI. This is to maintain a certain amount of liquidity in the system. What if there is a sudden rush of depositors to withdraw their money? If entire deposits have been issued as loans, there will be a liquidity problem. This can lead to a panic-like situation among stakeholders. Hence, banks should keep a minimum percentage reserve with RBI. This is called Cash Reserves Ratio (CRR). If the CRR percentage is reduced by the RBI, the amount available to loan out with the banks increases. But wait. There is more to it.  Banks also have to invest a proportion of the deposits in government bonds. In return, banks earn interest on their risk-free investment. This is known as the Statutory Liquidity Ratio (SLR). In return for these reserves, RBI pays a small percentage of interest to banks. It then constitutes as bank’s interest income. This is done to maintain a portion of deposits as emergency funds. If banks ever run into liquidity crises, RBI steps in and uses these reserves.

Banks also have to invest a proportion of the deposits in government bonds. In return, banks earn interest on their risk-free investment. This is known as the Statutory Liquidity Ratio (SLR). In return for these reserves, RBI pays a small percentage of interest to banks. It then constitutes as bank’s interest income. This is done to maintain a portion of deposits as emergency funds. If banks ever run into liquidity crises, RBI steps in and uses these reserves.

b. Other Income

Apart from interest income, banks earn revenue in the form of fees that they charge for various services. For example, banks also deal in foreign exchange operations and act as a broker and earn forex fees. They earn commission by selling mutual funds and insurance to their customers. It also includes income from various trading operations and other miscellaneous income. These other sources of income help them diversify their income stream rather than being dependent on interest income. So those are the major sources of income for a bank. Now let’s talk about the expenses.

c. Interest Expense

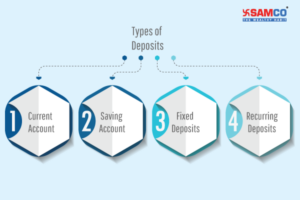

Banks pay a fixed percentage of interest on the amount deposited by the customers. This is their main expense which drives their cost. Consider these deposits as their raw materials. There are four types of deposits -  The rate of interest banks have to pay on current account and savings account (CASA) is relatively low than fixed deposits. Banks pay an interest of around 2% to 3% on saving accounts and 0% on current accounts. For fixed and recurring deposits, banks pay an interest of around 6% to 7%. CASA deposits let banks borrow funds at a lower rate. Hence, the higher the proportion of CASA, lower is the interest cost burden. For example, if a bank has a CASA Ratio of 30%, we can say that for every 100 rupees of deposits, 30 rupees have been through CASA. Pro Tip: If the CASA Ratio is high, it is a positive sign for investors. It means that banks are able to generate their raw material (money to loan) at a cheaper rate. A low CASA ratio means the bank heavily relies on costlier funding. Here are 5 Indian banks with the highest CASA Ratios as of September 2020 -

The rate of interest banks have to pay on current account and savings account (CASA) is relatively low than fixed deposits. Banks pay an interest of around 2% to 3% on saving accounts and 0% on current accounts. For fixed and recurring deposits, banks pay an interest of around 6% to 7%. CASA deposits let banks borrow funds at a lower rate. Hence, the higher the proportion of CASA, lower is the interest cost burden. For example, if a bank has a CASA Ratio of 30%, we can say that for every 100 rupees of deposits, 30 rupees have been through CASA. Pro Tip: If the CASA Ratio is high, it is a positive sign for investors. It means that banks are able to generate their raw material (money to loan) at a cheaper rate. A low CASA ratio means the bank heavily relies on costlier funding. Here are 5 Indian banks with the highest CASA Ratios as of September 2020 -

| Sr. No. | Name of the Bank | CASA Ratio (%) |

| 1 | Kotak Mahindra Bank | 57.1 |

| 2 | J&K Bank | 53.3 |

| 3 | IDBI Bank | 48.3 |

| 4 | HDFC Bank | 41.6 |

| 5 | IDFC First Bank | 40.4 |

Kotak Mahindra Bank has the highest CASA Ratio. In other words, 57.1% of its total deposits are being generated at a very low to minimal cost. You can find this data easily from the bank’s annual reports under their financial highlights’ section. So, how does the bank profit from this? To answer this question, we will have to understand a very important parameter that needs to be evaluated while analysing a bank.

d. Net Interest Income (NII)

The difference between bank’s interest income and interest expense is their profit. Let’s say that a bank lends at 7% interest and pays interest on deposits at 3.4%. The difference of 3.6% is bank’s net interest income. For example, HDFC Bank’s NII increased by 16.72 % in 2019-20.

| HDFC Bank | 2018-19 (in Rs.) ‘000 | 2019-20 (in Rs.) ‘000 |

| Interest Income | 1,05,16,07,400 | 1,22,18,92,915 |

| Interest Expense | 53,71,26,876 | 62,13,74,216 |

| NII | 51,44,80,524 | 60,05,18,699 |

Pro Tip: A large portion of the bank’s revenues is derived from Net Interest Income. Hence, always check at what rate is the bank’s NII growing. Higher the better. Compare the growth rate with its peers. Conduct a five-year trend analysis to have a better picture of the growth consistency. NII indicates how effectively is the bank conducting primary operations. So far, we understood how does a bank work and makes profits. This is on an absolute basis. But you cannot compare two different-sized banks on the basis of NII. For that, you must compare them on the basis of Net Interest Margin.

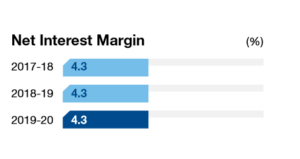

e. Net Interest Margin (NIM)

This is calculated by dividing NII by the average income earned from interest-producing assets. It is a profitability metric. This gives us an idea about the bank’s profitability on its interest income and their interest expenses. It is readily available in the bank’s annual report. For example, here is HDFC bank’s NIM from its 2019-20 Annual Report. You can find it under the key performance highlight system.  We can say that for HDFC bank, 4.3% is the net benefit of lending funds. Its capital is used efficiently. Monetary policies set by central banks majorly influence bank's net interest margins. They dictate whether consumers will borrow or save money. When interest rates are low, loans become cheaper. Thus, people are more likely to borrow money and less likely to save it. If borrowing increases, interest income for banks increases. This results in higher net interest margins. When interest rates are high, loans become costlier. Thus, people opt to save money rather than borrowing loans. If borrowing decreases, interest income for banks goes down. This decreases net interest margins. A positive NIM suggests that the bank is efficiently investing. Whereas a negative NIM suggests inefficient investing. Pro Tip: It is all connected. If the bank’s CASA ratio is high, NIM will be high. Analyse NII and NIM collectively to form a better opinion on a bank’s earnings performance. One element that can drastically affect NII and NIM is Non-Performing Assets.

We can say that for HDFC bank, 4.3% is the net benefit of lending funds. Its capital is used efficiently. Monetary policies set by central banks majorly influence bank's net interest margins. They dictate whether consumers will borrow or save money. When interest rates are low, loans become cheaper. Thus, people are more likely to borrow money and less likely to save it. If borrowing increases, interest income for banks increases. This results in higher net interest margins. When interest rates are high, loans become costlier. Thus, people opt to save money rather than borrowing loans. If borrowing decreases, interest income for banks goes down. This decreases net interest margins. A positive NIM suggests that the bank is efficiently investing. Whereas a negative NIM suggests inefficient investing. Pro Tip: It is all connected. If the bank’s CASA ratio is high, NIM will be high. Analyse NII and NIM collectively to form a better opinion on a bank’s earnings performance. One element that can drastically affect NII and NIM is Non-Performing Assets.

What are Non-Performing Assets (NPA)?

Imagine you have lent Rs. 5,000 to your friend. He promises to repay you the amount after 15 days. But it has been 5 months and he still hasn’t repaid. You eventually lose hope of getting your money back. If you had those 5,000 in your pocket, you could have done many things to create future value. But you can no longer use them. Similarly, if a borrower defaults on interest or principal payment, the bank’s asset (loan issued) is no longer profitable. They thus become a non-performing asset (NPA). This is the most important data which needs to be compared amongst banks. NPAs of a bank can affect banking operations and revenue. If you are able to correctly analyse NPA’s, you will have a fair idea of which bank performs better than its peers. So, straighten up, and let’s understand this in detail! Interest earned on loans is the main source of income for banks. But what if the borrower fails to repay the principal amount of defaults with an interest payment? A loan is classified as a non-performing asset when the repayment is overdue for more than 90 days.

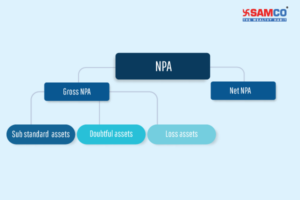

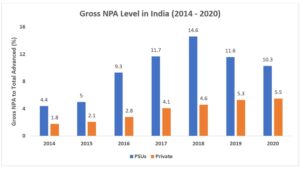

Imagine you have lent Rs. 5,000 to your friend. He promises to repay you the amount after 15 days. But it has been 5 months and he still hasn’t repaid. You eventually lose hope of getting your money back. If you had those 5,000 in your pocket, you could have done many things to create future value. But you can no longer use them. Similarly, if a borrower defaults on interest or principal payment, the bank’s asset (loan issued) is no longer profitable. They thus become a non-performing asset (NPA). This is the most important data which needs to be compared amongst banks. NPAs of a bank can affect banking operations and revenue. If you are able to correctly analyse NPA’s, you will have a fair idea of which bank performs better than its peers. So, straighten up, and let’s understand this in detail! Interest earned on loans is the main source of income for banks. But what if the borrower fails to repay the principal amount of defaults with an interest payment? A loan is classified as a non-performing asset when the repayment is overdue for more than 90 days.  Gross NPA is the total amount of NPAs without deducting the provisional amount. It consists of interest defaults as well as principal amount defaults. So, if a bank loans Rs. 50 lakhs to a start-up with a 10% interest rate, there is a risk that the bank might lose these Rs. 50 lakhs as well as the interest payments if the start-up fails to repay the amount. Banks classify Gross NPAs further into three categories - substandard, doubtful, and loss assets. a. Substandard assets Assets that are NPA for a period less than or equal to 12 months are substandard assets. b. Doubtful assets An asset that remains NPA for a period exceeding 12 months is a doubtful asset. They have a significantly higher risk level. c. Loss assets When a loss has been identified by an auditor and the amount has not yet been fully written off, it is classified as a loss asset. In other words, such an asset is considered uncollectible. Its record as an asset is not warranted although there may be some recovery value. In the financial year 2019-20, HDFC Bank reported a gross NPA of 1.26% which is one is the lowest in the banking industry. Pro Tip: It is very important to keep a track and analyse the bank's NPAs. Too many NPAs adversely affect a bank's liquidity and growth abilities. This is a big red flag. Have a look at the Public Sector bank’s (PSU) and Private Bank’s Gross NPA levels.

Gross NPA is the total amount of NPAs without deducting the provisional amount. It consists of interest defaults as well as principal amount defaults. So, if a bank loans Rs. 50 lakhs to a start-up with a 10% interest rate, there is a risk that the bank might lose these Rs. 50 lakhs as well as the interest payments if the start-up fails to repay the amount. Banks classify Gross NPAs further into three categories - substandard, doubtful, and loss assets. a. Substandard assets Assets that are NPA for a period less than or equal to 12 months are substandard assets. b. Doubtful assets An asset that remains NPA for a period exceeding 12 months is a doubtful asset. They have a significantly higher risk level. c. Loss assets When a loss has been identified by an auditor and the amount has not yet been fully written off, it is classified as a loss asset. In other words, such an asset is considered uncollectible. Its record as an asset is not warranted although there may be some recovery value. In the financial year 2019-20, HDFC Bank reported a gross NPA of 1.26% which is one is the lowest in the banking industry. Pro Tip: It is very important to keep a track and analyse the bank's NPAs. Too many NPAs adversely affect a bank's liquidity and growth abilities. This is a big red flag. Have a look at the Public Sector bank’s (PSU) and Private Bank’s Gross NPA levels.

Overall, we can observe that Indian’s NPA amount kept increasing from 2014 to 2018. It reached a peak of 11.2% in FY-2018. This was when many big corporate companies defaulted on their loan repayment. Public Sector banks show a very high level of NPA compared to Private. In 2015, PSB’s NPA levels almost is as much as the combined NPA levels of private banks in India. Private banks’ NPA levels are far less than PSUs which makes them a preferable option for investors. However, also note that there is a constant increase in their NPAs. Its Gross NPA of 1.8% rose to 5.5% by 2020. If the amount of NPA keeps rising, it could destroy customer’s deposits. To manage this risk, banks have to maintain a provision for bad assets in case of future losses. Higher the provision, the safer is the bank if it faces a stressful situation. Net NPA is simply the total bad assets (gross) minus the provision left aside. It is used as a measure of the overall quality of the bank’s loan book. For example, a bank loans out Rs. 100 Crores and the provisional amount set aside is Rs. 20 Crores. By the end of the financial year, the bank manages to collect Rs. 65 Crores only. Here, net NPA will be, gross NPA of 35 Crores - provision of 20 Crores = Net NPA = Rs. 15 Crores. Pro Tip: NPAs negatively affect their ability to generate adequate income and profitability. If a bank’s asset starts turning bad, their revenue and return on assets are directly affected. This is a red flag for investors. A low NPA level suggests that the bank has prudent credit evaluation policies and processes. Analyse a bank’s past NPA behaviors. Compare them with their peers. Higher NPAs threatens financial health.

How does NPA affect NII and NIM?

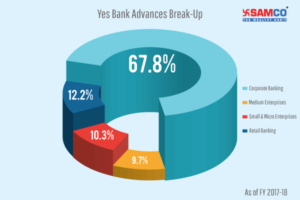

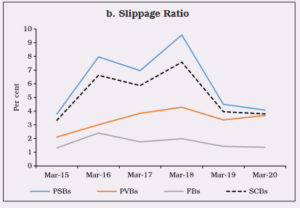

When good assets turn bad, the average interest-generating assets go down. This reduces interest income while the interest expenses remain the same. This directly affects their primary source of income. So, higher the NPA, less will be NII and NIM. NPA Adversity Learning and Examples: a. The Indian Economy enjoyed a boom phase from 2000-2008. Banks extensively issued loans to corporates with an expectation that the boom phases will benefit everyone. However, the 2008 financial crisis badly hit the economy and shook corporate profits pushing them to bankruptcy and other crisis. This further affected the NPA’s during the recession, especially for public sector banks. b. Yes bank suffered almost 90% downfall when the news of their high NPAs and poor financials broke out. Out of panic, customers rushed to withdraw their deposits. To control the situation, all the withdrawals were capped at Rs. 50,000. This further impacted many businesses’ cash flow. But, the devil is in the detail. If we analyse Yes bank’s advances break-up, we will find that about 67.9% of Yes Bank’s loans are offered to large corporates. Banks incur low costs if they lend funds to huge corporates. However, the risk factor cannot be ignored.  If a couple of such large borrowers default on their repayment, it could result in a very stressful situation for banks and the investors. Worst fears came true for Yes Bank They had financed couple of huge loans which ended up as NPA’s like IL&FS, Jet Airways, Anil Ambani Group, Essel Group, DHFL etc. Watch our case study on the entire Yes Bank saga. https://www.youtube.com/watch?v=aOskhHSGM4w&t=8s Pro Tip: When you are reading a bank’s annual report, check their loan issuing pattern. This will give you an idea about the risk they are taking or might face in the future. Covid-19 has induced uncertainty amongst many economic and global factors. This can deteriorate the asset quality of the banking system to a certain extent. In such unforeseen scenarios, the market sentiments are often low. In such times, it is important to closely monitor the bank’s NPA behavior. Check at which rate is the good loans turning bad. This is known as the slippage ratio. It helps us evaluate how much of a fresh NPA was added in a particular year or a quarter. Fresh slippage is the amount of how much of a bank’s advances turned bad in a year. Banks usually report this amount on a quarterly basis in their annual report or in a separate press release. A sharp increase in fresh slippage has a significant impact on the net profit of the bank. Low or no slippage shows a bank’s efficiency in handling its assets. Historically, Public Sector Banks have a very unstable slippage ratio. It increased in 2018 and followed a sharp fall in 2019.

If a couple of such large borrowers default on their repayment, it could result in a very stressful situation for banks and the investors. Worst fears came true for Yes Bank They had financed couple of huge loans which ended up as NPA’s like IL&FS, Jet Airways, Anil Ambani Group, Essel Group, DHFL etc. Watch our case study on the entire Yes Bank saga. https://www.youtube.com/watch?v=aOskhHSGM4w&t=8s Pro Tip: When you are reading a bank’s annual report, check their loan issuing pattern. This will give you an idea about the risk they are taking or might face in the future. Covid-19 has induced uncertainty amongst many economic and global factors. This can deteriorate the asset quality of the banking system to a certain extent. In such unforeseen scenarios, the market sentiments are often low. In such times, it is important to closely monitor the bank’s NPA behavior. Check at which rate is the good loans turning bad. This is known as the slippage ratio. It helps us evaluate how much of a fresh NPA was added in a particular year or a quarter. Fresh slippage is the amount of how much of a bank’s advances turned bad in a year. Banks usually report this amount on a quarterly basis in their annual report or in a separate press release. A sharp increase in fresh slippage has a significant impact on the net profit of the bank. Low or no slippage shows a bank’s efficiency in handling its assets. Historically, Public Sector Banks have a very unstable slippage ratio. It increased in 2018 and followed a sharp fall in 2019.

Source: RBI 2019-20 Trend Report

Search for banks that undertake measures to ensure that their NPA level does not increase. This brings us to our next question. How to analyse if a bank is taking safety precautions to maintain its asset quality? Let’s understand that in our next point. How do we analyse if operational efficiencies have enabled banks to maintain healthy levels of profitability? Banks usually set aside a portion of their profits as a reserve against bad loans. These funds are set aside to cover up losses if some of their loans turn into NPAs. They are known as Provision Coverage Ratio (PCR).  A high PCR ratio (ideally above 70%) means that the bank is financially stable. Banks report this percentage in their annual report. It suggests that most asset quality issues have been taken care of in advance in case of casualties. Therefore, higher PCR is better. Earlier, RBI had prescribed a benchmark PCR of 70% of gross NPAs. There is no such benchmark now. If banks are earning good profits, it is ideal for them to increase their PCR. Building up such buffer is useful when a bank’s NPA increases quickly. Along with a provisional buffer, banks also maintain a capital buffer to be prepared in case of a financial crisis. This is known as Capital Adequacy Ratio (CAR) or Capital-to-Risk Weighted Assets Ratio (CRAR).

A high PCR ratio (ideally above 70%) means that the bank is financially stable. Banks report this percentage in their annual report. It suggests that most asset quality issues have been taken care of in advance in case of casualties. Therefore, higher PCR is better. Earlier, RBI had prescribed a benchmark PCR of 70% of gross NPAs. There is no such benchmark now. If banks are earning good profits, it is ideal for them to increase their PCR. Building up such buffer is useful when a bank’s NPA increases quickly. Along with a provisional buffer, banks also maintain a capital buffer to be prepared in case of a financial crisis. This is known as Capital Adequacy Ratio (CAR) or Capital-to-Risk Weighted Assets Ratio (CRAR).

What is Capital Adequacy Ratio (CAR)? Why is it important?

It particularly measures the financial risk of banks. CAR examines the available funds with banks in relation to extended credit weighted by exposure to various risks. In other words, it ensures credit discipline in a bank and protects the depositors. It analyses if the bank can absorb a reasonable amount of loss. Thus, this ratio becomes very important while analysing a bank's stock. It further promotes stability and efficiency in the financial system. Capital Adequacy Ratio = (Tier I Capital funds + Tier 2 Capital funds / Risk-weighted assets) Tier-1 capital absorbs losses without a bank being required to terminate trading. It is easily available to cushion losses sustained by a bank. It consists of equity capital, ordinary share capital, intangible assets, and audited revenue reserves. Tier-2 capital absorbs losses in the event of bank liquidation. If the bank loses all its tier 1 capital, tier-2 capital is used to absorb losses. It provides a lesser degree of security to depositors. Thus, tier-2 is observed as less secure than tier-1. It comprises unaudited retained earnings, unaudited reserves, and general loss reserves. For Indian private sector banks, RBI has mandated the minimum requirement of Tier-I capital ratio at 8.875%. Risk-weighted assets are calculated by studying bank loans and assessing risks. Weights are then assigned depending on each factor. It takes into account credit risk, market risk, and operational risk. The ratio is difficult to calculate as enough information is not easily available. However, these figures are easily available in the company’s annual report. Pro Tip: If a bank has a good CAR, it means that it has enough capital in the buffer to absorb potential losses. The bank has less risk of becoming insolvent and losing depositors’ money. It is financially strong. This is a positive sign for investors. The RBI has set the minimum capital adequacy ratio at 9% for banks. A CAR below 9% means that the bank does not have sufficient cushion. The chances of banks running into insolvency during stressed periods are high.

Provision Coverage Ratio vs Capital Adequacy Ratio (PCR vs CAR)

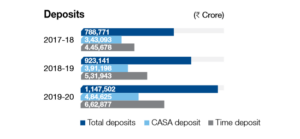

Both these ratios provide a cushion to banks in case of financial crises. Provisioning Coverage Ratio (PCR) is the percentage of funds that a bank sets aside to cover bad-debt related losses. Capital Adequacy Ratio manages the bank's capital to its credit exposure. It indicates the position of capital adequacy of a bank. In simple words, one takes care of the NPAs while the other looks after credit efficiency. However, a high CAR reduces a bank’s ability to lend funds. The capital set aside cannot be used further as advances. The capital could have been used as advances to earn future interest income. By reserving funds, it slows down bank’s growth in the long run. Thus, banks usually set aside a greater portion during the years when they earn higher profits. This helps them create a buffer to face financial shocks. It saves them from insolvency or bankruptcy. This is how banks prepare themselves to face any kind of risk. However, one thing to understand is that they can prepare sufficient reserves only if they earn better profits. So, it is important for banks to churn out the best from their assets. To decode bank’s asset qualities, we will have to look at their balance sheet. Deposits by the customers are the largest liability for the bank. Although they fall under liabilities, they are significant for banks to lend capital as loans. If a bank doesn't have enough deposits, lending will slow down. This further slows down growth if enough capital is not available in the system. Banks might have to borrow money (take loans) from RBI to meet the general public's loan demand. This is a costly way to generate funds and can affect the NII. Pro Tip: In their annual report's notes to accounts, look at deposits’ breakdown. We earlier saw how banks can generate funds at a cheaper rate with a higher CASA ratio. Observe which type of deposit is growing. Is it the current and savings account? Or is it fixed or recurring deposits? Here is HDFC bank's deposit breakdown from their annual report 2019-20.  In 2018-19, HDFC bank’s total deposits grew by 17.03%. In 2019-20, the growth rate was 24.30%. In 2018-19, CASA deposits grew by 14.02%. In 2019-20, the growth rate was 23.88%. Whereas, in 2018-19, time deposits grew by 19.36%. In 2019-20, the growth rate was 24.61%. We can observe that the total deposits’ and CASA deposits’ growth rate has improved by a healthy amount. This is a positive sign for investors. Another element to evaluate in the balance sheet is the total advances or the loans issued by the bank. Advances is the largest assets of the bank. They are their bread and butter on which they earn interest which ultimately makes the entire monetary cycle work. Here is HDFC bank’s advances from their 2019-20 annual report –

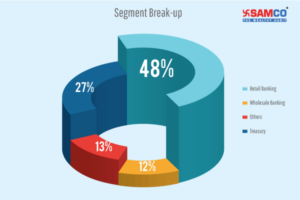

In 2018-19, HDFC bank’s total deposits grew by 17.03%. In 2019-20, the growth rate was 24.30%. In 2018-19, CASA deposits grew by 14.02%. In 2019-20, the growth rate was 23.88%. Whereas, in 2018-19, time deposits grew by 19.36%. In 2019-20, the growth rate was 24.61%. We can observe that the total deposits’ and CASA deposits’ growth rate has improved by a healthy amount. This is a positive sign for investors. Another element to evaluate in the balance sheet is the total advances or the loans issued by the bank. Advances is the largest assets of the bank. They are their bread and butter on which they earn interest which ultimately makes the entire monetary cycle work. Here is HDFC bank’s advances from their 2019-20 annual report –  Total advances constitute of 66% of total bank assets. Thus, it becomes critically crucial to evaluate this figure. Pro Tip: Analyse who is the bank issuing loans to. This is an important detail an investor needs to analyse. If the bank management makes poor decisions repeatedly then chances of these loans turning into an NPA are high. Hence observe the advances section under the asset side of the balance sheet. It includes loans issued within India as well as outside India. This can be in the form of cash credits, overdrafts, term loans, loans to other banks, loans to retailers as well as government. When you analyse the notes to advances, you will find the further breakdown to secured and unsecured loans. Evaluate how sensitive is the bank to market risk. Sensitivity to Market Risk records the changes in interest rates, foreign exchange rates, commodity prices, or equity prices. For most banks, market risk essentially indicates exposure to changing interest rates and the credit risk to sensitive sectors. Credit Risk to Sensitive Sector Credit risk occurs when borrowers fail to repay their loans. It is the biggest risk for banks. Banks always need to be prepared for credit risk challenges. If we want to invest our money in the banking sector, we need to analyse which bank is less sensitive to risks. Banks’ exposure to the capital market and real estate is considered very sensitive to risk. This is because of the constant fluctuation in prices. Pro Tip: To decrease market risk, diversification of investments is important. Review the bank's investment breakdown and its revenue sources. Are they dependent on a particular source? Or does the bank have a well-diversified portfolio? For example, here is HDFC Bank’s Revenue Mix.

Total advances constitute of 66% of total bank assets. Thus, it becomes critically crucial to evaluate this figure. Pro Tip: Analyse who is the bank issuing loans to. This is an important detail an investor needs to analyse. If the bank management makes poor decisions repeatedly then chances of these loans turning into an NPA are high. Hence observe the advances section under the asset side of the balance sheet. It includes loans issued within India as well as outside India. This can be in the form of cash credits, overdrafts, term loans, loans to other banks, loans to retailers as well as government. When you analyse the notes to advances, you will find the further breakdown to secured and unsecured loans. Evaluate how sensitive is the bank to market risk. Sensitivity to Market Risk records the changes in interest rates, foreign exchange rates, commodity prices, or equity prices. For most banks, market risk essentially indicates exposure to changing interest rates and the credit risk to sensitive sectors. Credit Risk to Sensitive Sector Credit risk occurs when borrowers fail to repay their loans. It is the biggest risk for banks. Banks always need to be prepared for credit risk challenges. If we want to invest our money in the banking sector, we need to analyse which bank is less sensitive to risks. Banks’ exposure to the capital market and real estate is considered very sensitive to risk. This is because of the constant fluctuation in prices. Pro Tip: To decrease market risk, diversification of investments is important. Review the bank's investment breakdown and its revenue sources. Are they dependent on a particular source? Or does the bank have a well-diversified portfolio? For example, here is HDFC Bank’s Revenue Mix.

Source: HDFC Bank's Annual Report 2019-20

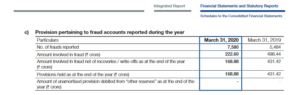

Over the past years, one reason why NPAs of Indian banks increased is because of huge corporate frauds and scams. Single negative news on the part of the top-level management can break the entire system. Operational risk has emerged as a major source of risk. This makes evaluating management capabilities and qualifications very important. In 2018, before things went south for Yes Bank, customers were happy with the bank’s operation. However, on 17th September 2018, RBI asked Rana Kapoor - Managerial Director of Yes Bank to end his tenure on 31st January 2019. When the news broke out, stakeholders were quick to smell something bad behind RBI’s statement. The company’s stock price started tumbling. When the NPA figures were made public, the stock price further tumbled which wiped out Rs. 22,000 crores from Yes Bank’s market capitalsation in a single day. This ultimately erodes investor’s confidence. ICICI Bank’s Chanda Kochhar also had to quit in October 2018 over accusations regarding fraudulent loans to the Videocon Group. Pro Tip: read bank’s annual reports and press releases where they present their fraud records. Though these records are often sugar-coated in the annual reports, it gives us an idea to compare and evaluate a banking stock further. Here is HDFC Bank’s frauds and scams report –

HDFC Bank’s Annual Report 2019-20

Observe how the number of reported frauds went up by 38% but the amount involved in frauds in March 2020 fell about 55.34% compared to March 2019. Evaluating these reported numbers speaks volumes about the quality of the management. Another way to evaluate the management, industry, or a particular bank is by conducting a SWOT analysis. It provides us a concise overview of the internal as well as external factors that can affect a bank's growth.

SWOT Analysis

Strengths of a bank: Read about the recent achievements of a particular bank in their latest annual report. A bank’s strength may include – a. Excellent top-level executives We discussed how important it is for a bank to have the best management system. This helps the bank to improve and grow in the future. For example, HDFC Bank has one of the steadiest top management teams who has been associated with the bank for more than a decade. In 2018, Yes bank's management was constantly in news for its poor management. We all know how the bank plunged within days. b. Diversified business model Diversification makes banks less sensitive to sector-specific and concentration risks. For example, Kotak Mahindra Bank has a well-diversified business portfolio model. They operate across various domains like lending, insurance, asset management, capital market. This helps the bank to maintain steady earnings growth. c. Financial products Banks with a wide array of products like accounts, deposits, cards, loans, insurance, forex, and investment are stronger than others Their strengths also include high client retention, low staff turnover, and overhead, better credit ratings, etc. Weaknesses a. High Levels of NPAs NPAs are the bane of the banking sector. Developing countries such as India face instances of high NPAs. This amount eventually affects the entire credit system of the banks. They have a crippling effect. Over the years, the NPA levels are rising due to various frauds and scams. It is management's responsibility to have a strong system to control their NPAs to maintain efficiency. b. Covid-19 and other uncertainties Being a highly sensitive sector, banks must always be ready to face economic crises. For example, Covid-19 induced uncertainty amongst global factors. Such uncertainty can deteriorate the asset as well as earning quality of the banking system. In such scenarios, the market sentiments are often low. Banks prepare high provisions to face future losses. These provisions cannot be used for other operations and hence cannot generate further profits. c. Retaining Talents Banks thrive on the strength of their human resources. One of the most essential factors that can make or break a company is the performance of their employee. However, banks face the problem of employee retention, especially Public Sector Banks. Various factors lead to employees quitting the organisation. For example, lack of work-life balance, lagged succession planning, poor pays, no defined working hours for bank employees, etc. Opportunities a. Technology Implications The banking sector has evolved in many folds over the past few years. Banks have a huge opportunity to further adapt these technology innovations to increase their efficiency. b. Rural Expansion Opportunities Banks have a huge opportunity to penetrate the rural area's which are still untapped. Banks can grow their customer base by expanding into villages. Other banking opportunities include better reforms, growing economic, global political stability, etc. Threats a. Increasing competition in the finance market Various new services and products are being introduced and sold in unique ways. It is very important for financial industries to keep up with the competition and offer new services to their customers. b. The slowdown in the economy The economic slowdown is one of the biggest threats to every business. Banks ultimately face huge financial crises as a result of the slowdown. Their threats also include changes in banking norms, high unemployment, frequent changes in interest rates, etc. c. Data leaks and hacking

This detailed article on how to analyse a company using SWOT analysis will help you understand each element in detail. It also consists of questions you should ask to derive at a certain conclusion. Once you are done analysing and evaluating asset, earnings, and management quality, we come to the main question –

When to invest in banking stocks?

The best time to invest in a bank is when it is undervalued. It means that the fundamentals of the bank are strong. But due to recent news or event, the stock is not trading at its intrinsic value. The potential of the stock to grow is high if it undervalued. Pro Tip: Warren Buffett said that if the fundamentals are strong, you must learn how to ignore the outside noise. This is one of the main points of his investment strategy. There are many valuation parameters that determine whether a stock is cheap or expensive. They are especially relevant when the market is growing or is at a peak. One of them is the Price to Book ratio (PB Ratio). To value a banking stock, PB ratio is the best tool. Bank’s assets and liabilities are normally marked to market. They are either very liquid instruments or their value is easily determined. For example, advances and deposits. Hence, PB Ratio is the most important parameter to check and compare before drawing conclusions.

Price to Book Value Ratio (PB Ratio)

Book value refers to the value of a company’s assets minus the liabilities. Price to book value is the price of a company divided by its book value. It compares the bank’s market capitalization to its book value. This ratio has less volatility which makes the valuation more stable and reliable. PB Ratio = Market Price of the Share / Book Value per Share It is a perfect valuation metric for banks because it captures how efficiently the funds or the assets are being utilized. A high PB ratio generally means that the stock is trading at a much higher valuation than its book value and vice versa. For example, Kotak Mahindra Bank’s PB Ratio is 5.32 as of May 2021. This means investors are paying 5.32 times more for a company’s assets to buy a share. Ideal way to analyse a bank’s PB Ratio is by comparing it with its own historical ratio or the industry average. Let’s understand this with the industry average. The average PB ratio of private banks and public banks is 1.83 and 0.48 respectively. Here are three banks with the highest PB Ratio. These banks are well above the industry average and are over-valued.

| Name | Ownership | PB Ratio |

| AU Small Finance | Private | 7.2 |

| Kotak Mah. Bank | Private | 5.32 |

| HDFC Bank | Private | 4.7 |

Top three banks with lowest PB Ratio.

| Name | Ownership | PB Ratio |

| Bank of India | Public | 0.56 |

| Central Bank | Public | 0.53 |

| Dhanlaxmi Bank | Private | 0.46 |

Bank of India and Central Bank are around Public sector bank’s Industry average and hence are fairly priced. Dhanlaxmi Bank (Private Bank) is well below its industry average and is under-valued. In other words, we can say that Dhanlaxmi bank is the cheapest bank, and AU Small Finance is relatively expensive. Price to book value can also be negative. One of the main reasons for a negative PB ratio is having a consistent negative cash flow. As of May 2021, no Indian Banks have a negative PB Ratio. Read How to Use Price to Book Value (PB Ratio) for Stock Analysis explained in detail. However, a low PB ratio could also mean that there are foundational issues because of which it is not showing earnings. The management can try to manipulate the numbers. Hence, the investor must compare the banks current PB ratio with historical average. If the current PB ratio is trading below historical average then the bank could be considered as undervalued. Apart from this you can also look at other metrics along with PB Ratio. To form an effective perspective, use PB Ratio with Return on Equity (ROE). These two parameters together offer a better insight into the bank’s growth prospects.

- ROE Formula = Net Income / Average Shareholder’s Equity

- PB Ratio = Market Price of the Share / Book Value Per Share

PB ratio compares a company’s stock price with the book value of its assets. Whereas ROE measures the profits made for each rupee from shareholders’ equity. It shows the firm’s ability to turn equity investments into profits. Pro Tip: If ROE is high along with a low PB Ratio, it indicates that the bank is under-valued. And if ROE is low along with high PB Ratio, it indicates that the bank is over-valued. That is because ROE captures the aspect of return on assets and also return on capital employed. PB Ratio misses out to capture these elements. This gives us a fair idea about the bank’s potential future earnings. Comparing the top five private banks according to their market capitalisation.

| Name | PB Ratio | ROE % |

| HDFC Bank | 4.7 | 18.05 |

| ICICI Bank | 3.62 | 14.95 |

| Kotak Mahindra Bank | 5.32 | 14.88 |

| Axis Bank | 2.63 | 8.33 |

| IndusInd Bank | 2.31 | 8.6 |

*as of March 2021 Kotak Mahindra banks seems to be over-valued when compared to other private banks. With ROE of around 14%, ICICI bank is undervalued in comparison to Kotak Mahindra Bank. There can be situations when PB Ratio might indicate that a stock is under-valued but might have a negative ROE. For example -

| Public Sector Banks | PB Ratio | ROE % |

| Indian Overseas Bank | 1.67 | -52.49 |

| Canara Bank | 0.61 | -5.04 |

| Bank of India | 0.55 | -7.03 |

| Union Bank of India | 0.72 | -10.28 |

The average PB ratio of public banks in India is 0.48. PB ratio of PSU banks in our example is around the industry average which makes them fairly valued stocks. However, look at their ROE. A negative ROE suggests that the banks are incurring losses on their investments. This does not make them ideal investment options. A negative or a declining ROE suggests that the management is making poor decisions on reinvesting capital in unproductive assets. Pro Tip: One drawback about ROE is that it measures equity capital only. It does not capture debt capital. To fill this gap, investors should observe Return on Assets (ROA) of a bank. ROA measures both, equity and debt capital.

Returns on asset (ROA)

ROA is the profit a bank is able to generate on its total assets. It is calculated by dividing net income by its total assets. It helps us understand if the management is using its assets efficiently to generate more income. When the quality of asset improves, benefits like liquidity and its risk capacity also improves. The higher the ROA, the more productive and efficient a management is in utilizing economic resources. A lower ROA means that the bank is not able to utilise assets efficiently. Negative ROA implies the bank’s assets are bearing negative returns (losses). This is a red flag for investors. A good banking system can absorb adverse conditions whereas a poor system can lead to financial crisis. Therefore, banks need to improve continuously and be ready to face any difficult situation.

Where can we find all the data to analyse a bank?

Primary Sources

- Annual reports of banks

- Investor presentation reports

- Conference call transcripts

- Quarterly and half-year reports

- RBI website

Additional Sources

- Company's website

- National Stock Exchange (NSE) website

- Bombay Stock Exchange (BSE) website

- Samco’s Stock Page

Using Samco’s stock page, you can find the latest valuations for each listed company along with stock ratings. Check every bank’s ranking before making any investment decisions.

Checklist for investors

1. Understand the banking business model and collect all relevant data to analyse banking sector. This includes all financial ratios and parameters we discussed in this article. Always remember to check the Price to Book Value ratio. 2. Conduct a comparative ratio analysis with peer banks and their industry average. Put major emphasis on – a. Non-Performing Assets b. Net Interest Income and Net Interest Margin c. Capital Adequacy Ratio These three ratios have the power to impact every aspect of the bank. 3. Understand the bank’s position by evaluating how sensitive they are to risk with respect to its competitors. 4. Check qualitative factors by performing SWOT analysis and by analysing the top-level executives. 5. Check if the bank is in the news. If so, understand why and how it can impact the bank’s future performance. 6. Check if there are any new regulations or reforms. For example, changes in cash reserve ratio (CRR), statutory liquidity ratio (SLR) and repo rates can affect banking business. Banks originally started as a place where people can safely store their money. Today, banks have developed into digital entities. they offer financial services and products which we can access from the comfort of our couch.  Analysing banking stocks can be a time-consuming process. But, keeping these points in mind will help you form a strong opinion on any banking stock. It might look long and exhausting process but is absolutely essential. All you need to do is dedicate some time to researching an investment option rather than rely on unreliable tips. If you follow the steps mentioned above then I am certain you can analyse a banking stock easily. This is the best way to ensure you make the best decision for the money you invest. Using Samco’s stock page will help you solve half of your trouble. Samco is constantly working with dedication to provide you the best tools to improve your wealth and finances. You can access latest financial data, important ratios and valuations, pros & cons and many more details on your screen. You can also check which stock is rated as 1-star and which is a 5-star stock. This helps investors make their investment analysis process better and easier. Conduct your own independent analysis today! Take your first step towards stock market trading by opening a FREE Demat account with Samco.

Analysing banking stocks can be a time-consuming process. But, keeping these points in mind will help you form a strong opinion on any banking stock. It might look long and exhausting process but is absolutely essential. All you need to do is dedicate some time to researching an investment option rather than rely on unreliable tips. If you follow the steps mentioned above then I am certain you can analyse a banking stock easily. This is the best way to ensure you make the best decision for the money you invest. Using Samco’s stock page will help you solve half of your trouble. Samco is constantly working with dedication to provide you the best tools to improve your wealth and finances. You can access latest financial data, important ratios and valuations, pros & cons and many more details on your screen. You can also check which stock is rated as 1-star and which is a 5-star stock. This helps investors make their investment analysis process better and easier. Conduct your own independent analysis today! Take your first step towards stock market trading by opening a FREE Demat account with Samco.

Easy & quick

Easy & quick

Leave A Comment?