In this article, we will cover,

-How balanced or hybrid mutual funds work?

-Characteristics of equity & debt-oriented balanced mutual funds

-Who should Invest in Balanced Funds?

-Balanced funds can be used for intermediate financial goals like,

-Things an Investor should consider while investing in Balanced or Hybrid Funds

-Top performing Balanced Funds in India

How Balanced or Hybrid Mutual Funds work?

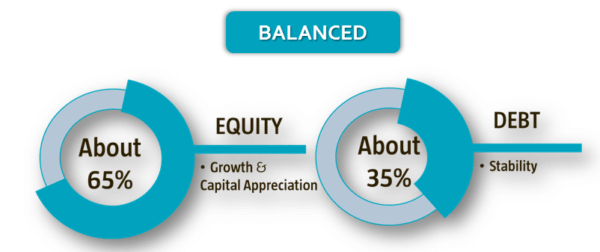

A Balanced fund basically invests in a diversified portfolio. These funds typically invest in a mix of equity stocks and debt securities. In the equity portion, they invest in shares of various companies from a diverse range of sectors with market capital such as large-cap, mid-cap, and small-cap. For the debt portion, they invest in the debt securities such as Government bonds, Treasury bills of Reserve Bank, Municipal bonds, Commercial papers issued by companies, Non-convertible debentures, Certificates of deposits issued by banks, and other similar securities. So this is how a balanced fund creates a perfect mix between risky asset class such as equity to create wealth in the long term and a comparatively safer asset class which is represented by the debt portion. This ideal blend of balanced funds fetched returns of around 11% to 13% compounded yearly.

In this article, we will cover,

-How balanced or hybrid mutual funds work?

-Characteristics of equity & debt-oriented balanced mutual funds

-Who should Invest in Balanced Funds?

-Balanced funds can be used for intermediate financial goals like,

-Things an Investor should consider while investing in Balanced or Hybrid Funds

-Top performing Balanced Funds in India

How Balanced or Hybrid Mutual Funds work?

A Balanced fund basically invests in a diversified portfolio. These funds typically invest in a mix of equity stocks and debt securities. In the equity portion, they invest in shares of various companies from a diverse range of sectors with market capital such as large-cap, mid-cap, and small-cap. For the debt portion, they invest in the debt securities such as Government bonds, Treasury bills of Reserve Bank, Municipal bonds, Commercial papers issued by companies, Non-convertible debentures, Certificates of deposits issued by banks, and other similar securities. So this is how a balanced fund creates a perfect mix between risky asset class such as equity to create wealth in the long term and a comparatively safer asset class which is represented by the debt portion. This ideal blend of balanced funds fetched returns of around 11% to 13% compounded yearly.

Balanced funds mainly come in 2 categories:

- Equity-oriented balanced funds

- Debt-oriented balanced funds also known as Monthly income plans (MIP)

Characteristics of equity & debt-oriented balanced mutual funds

1.Equity-oriented Balanced funds

Equity-oriented balanced funds aim to achieve wealth appreciation in the long term through investment in equities and generate income through interest income in the short term via investment in debt securities such as government bonds, commercial papers, debentures, etc. and generate good returns by a perfect blend of an equity & debt portfolio. The fund manager allocates investor’s money in different proportions in equity and debt instruments based on the investment mandate of the fund.

The equity component of the fund comprises equity shares of companies across various industries like Infrastructure, FMCG, Banking & Finance, Pharma, Real estate, IT, Automobiles, etc. The debt component of the fund constitutes an investment in fixed-income instruments like government bonds, commercial papers, corporate debentures, treasury bills, etc. The fund manager may buy or sell shares and other securities to take advantage of market movements.

2.Debt-oriented balanced funds

Debt-oriented balanced mutual funds invest predominantly in debt instruments. These funds are preferred by investors who want a relatively safer investment avenue rather than investing their entire principle in equities but at the same time, they can also want some flavor of equity to taste the market momentum so that they don’t miss out on the rally in the equity markets. These debt-oriented mutual funds, such as Monthly Income Plan (MIP), invest approx. 75%-80% of their total collected capital into debt securities such as government bonds, treasury bills, commercial papers, etc. The remaining 25%-20% of the corpus is invested in equities to take benefits of market movements as mentioned earlier. This would allow the fund to generate higher returns than regular debt funds because of the equity component. MIPs, as the name suggests, should not be treated as a mere monthly income investment. The name can be misleading to new investors. Consider MIPs to be hybrid funds that invest in a mixture of the portfolio that mostly comprises of debt and some amount in equities. MIPs comes in two options, namely “Dividend option” and “Growth option.” In dividend option, MIPs provide regular income to the investor in the form of dividends and interest income which they earn through investment in debt securities & equity shares. An investor can choose the frequency of dividends as per his requirements, which can be monthly, quarterly, half-yearly or annually. But the dividend income from a debt-oriented the instrument is subject to dividend distribution tax (DDT) of approx. 28.82% which is deducted by AMC at source & after-tax dividend amount which comes in the hands of investors is comparatively less. This is the reason why many financial advisors suggest investors not go with this option nowadays. Now, the question is what if the investor requires monthly or quarterly cash flows like he would have received in the form of dividends if he had opted for the dividend option? There’s a solution for it. We would advise investors to go with the Growth option in MIP. Growth option doesn’t pay out dividends but lets that investments grow in the fund’s corpus. For his cash flow requirements, an investor can select a Systematic Withdrawal Plan (SWP) in Growth option. Under SWP, he can select a fixed amount, let's say 10,000/- per month, which will be credited to his bank account on a fixed date per month irrespective of market movements. He can select the frequency of the cash flows as per his requirements i.e. monthly, quarterly, half-yearly, etc. SWP from Growth option rather than the dividend from the dividend option is not only free of Dividend distribution tax (DDT) but also gives indexation benefit on the capital gains arising after completion of 3 years from the date of investment. This will fulfill his liquidity needs on a regular basis. The investor can expect a return of 9% to 11% per year in this 80:20 debt-equity blended fund.Who should Invest in Balanced Funds?

Balanced funds are considered as safer bets than pure equity funds & suitable for investors who do not want to invest 100% of their capital in equities and prefer lower risk. These funds fetch higher returns than pure debt funds which invests the entire corpus in fixed-income instruments. Balanced funds are favorite among conservative investors. New investors who are eager to take exposure in equity markets can think of balanced funds as the first step towards achieving their financial goals. As these are an ideal blend of equity and debt, the equity component helps to ride the equity up-move as equity is the most profitable asset class over long-term. At the same time, the debt component of the fund provides a cushion against extreme market turbulence. In that way, an investor receives stable returns instead of a total burnout that might be possible in case of pure equity funds when markets do not perform well.Balanced funds can be used for intermediate financial goals like,

- Funding higher education of kids

- Vacation abroad

- Marriage

- Buying a dream home

- Buying a car

- Retirees choose to invest in balanced funds and go for a dividend option in the funds which gives regular dividends to supplement their post-retirement income.

Things an Investor should consider while investing in Balanced or Hybrid Funds:

Before investing in Balanced mutual funds, the investor needs to consider these 4 things in order to arrive at the right decision.1.Risk

An investor should not assume that the balanced funds are completely risk-free. Any instrument which invests in equity markets will have some kind of risk because of the nature of equity. It is less risky than pure equity funds that invest 100% in equity only, but you need to be cautious and rebalance the portfolio on a regular basis. Many balanced funds declare regular dividends, one of the most prominent reasons why investors invest in these mutual funds. However, investors should understand that these funds might not be able to declare dividends during market downturns if they are unable to make enough profits to distribute as dividends.2.Return

Balanced funds don’t guarantee returns. The performance of underlying shares & securities affect the Net Asset Value (NAV) of these funds and may fluctuate due to market movements. Balanced funds usually give returns around 11% to 13% compounded annually which depends on the equity allocation which the fund has made as per its investment objective.3.Investment Horizon

Balanced funds are ideal for a medium-term investment horizon of 3 to 6 years. An investor can expect his initial capital to double in 6 to 7 years time horizons depending on the market movement.4.Tax on Gains

Both equity oriented and debt oriented balanced fund has different tax treatment which is explained below. As per the latest amendment in the Union Budget 2018, in case of equity-oriented balanced funds, long-term capital gains or LTCG (holding period ≥ 1 year) in excess of Rs 1 lakh are taxed at the rate of 10% whereas short-term capital gains or STCG (holding period < 1 year) on equity component are taxed at the rate of 15%. In case of debt-oriented balanced mutual funds, long term capital gains (holding period > 3 years) are taxed at the rate of 20% after indexation and 10% without the benefit of indexation. Short term capital gains (holding period ≤ 3 years) are added to the investor’s income and taxed according to his income slab.5.Cost

Balanced funds would charge a fee for managing investor’s portfolio like all mutual funds, which is known as the expense ratio. The expense ratio, better known as annual fund operating charges, indicate fees charged by the Asset Management Company (AMC) in order to pay for their expenses such as hiring of highly qualified and experienced fund manager, setting up technical expertise to track the changes in the markets, custodian fees and legal charges. Expense ratio is adjusted by AMC in the NAV of the fund itself. Investors are not required to pay anything separately.Top performing Balanced Funds in India:

While selecting a fund, an investor needs to analyze the fund from different parameters. There are various quantitative and qualitative parameters which can be used to arrive at the best-balanced funds as per his requirements. Additionally, he needs to keep his risk appetite, investment horizon and financial goals in mind as pointed earlier. The following table represents the top performing balanced funds in India based on the past 5 year returns. Investors may choose the mutual funds based on a different investment horizon like 10 years returns. They may include other criteria like fund manager’s experience, consistency, financial ratios as well. Following is the list of top performing balanced funds as per recent data. For more detailed information about best performing balanced funds you can visit our website Rankmf.com to know “Kaunsa mutual fund sahi hai!!”| Sr.No | Name of Fund | Minimum Investment | 1 Year Returns | 3 Year Returns | 5 Year Returns | Returns Since Inception |

| 1 | Edelweiss Balanced Advantage Fund - Growth Option | 500 | 25.49% | 11.21% | 11.68% | 10.50% |

| 2 | Canara Robeco Equity Hybrid Fund Regular Growth | 1000 | 21.49% | 11.50% | 13.55% | 11.45% |

| 3 | Motilal Oswal Equity Hybrid Fund-regular Plan Growth | 500 | 17.88% | - | - | 14.64% |

| 4 | Union Balanced Advantage Fund Regular Plan - Growth | 2000 | 23.28% | 11.67% | - | 11.63% |

| 5 | Tata Balanced Advantage Fund Regular Plan Growth | 150 | 17.55% | - | - | 13.49% |

Easy & quick

Easy & quick

Leave A Comment?