Deepak Nitrite Limited (DNL) is a prominent Indian chemical intermediates company recognized for its diverse product range and responsible manufacturing practices. The company's products cater to a wide array of industries, including dyes and pigments, agrochemicals, pharmaceuticals, plastics, textiles, paper, home and personal care, and petroleum derivatives. It is the largest producer of phenol, acetone, IPA, and sodium nitrite in India.

Today, the company announced its Q3FY25 results, and the share price reacted adversely, correcting by more than 15%. Here’s the reason for the fall:

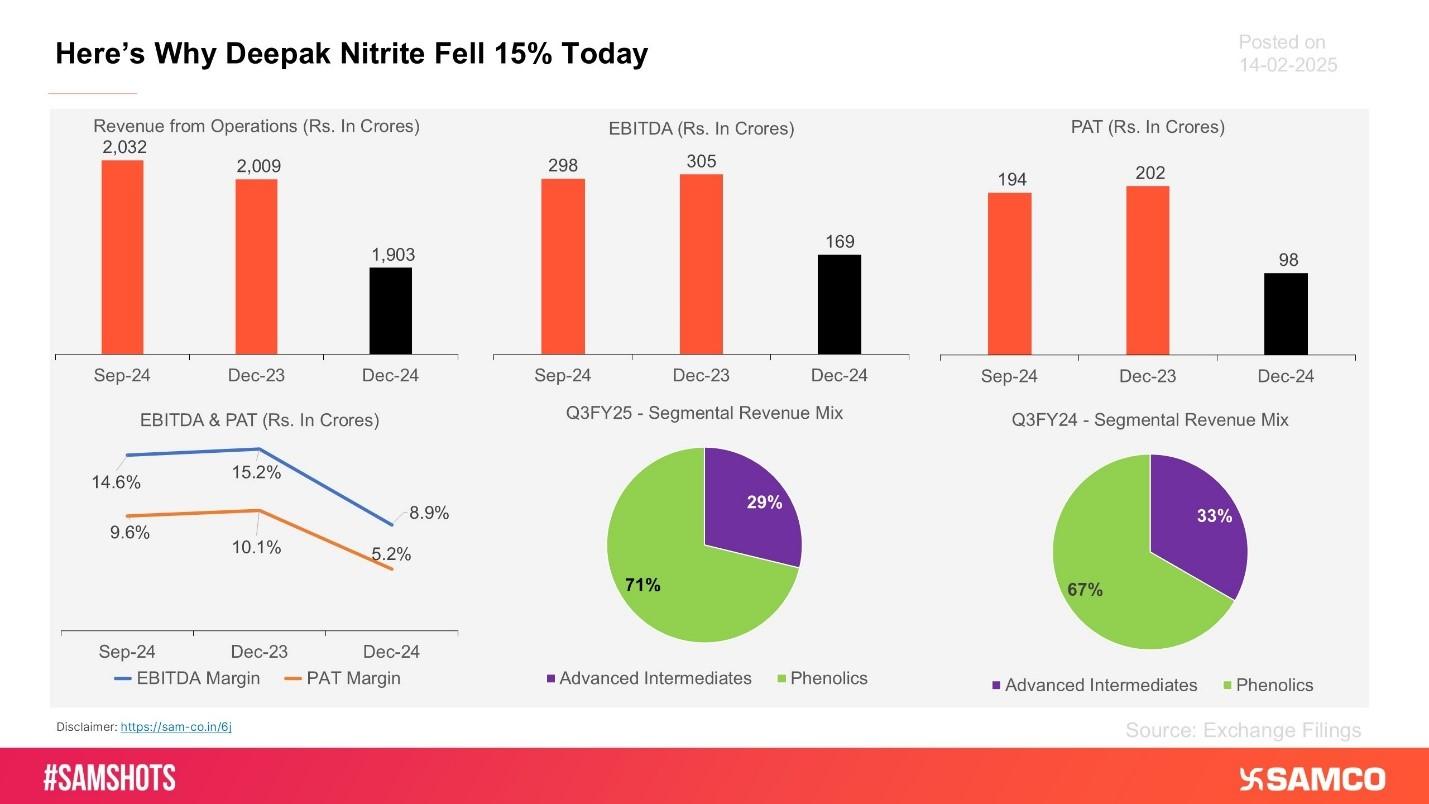

The consolidated revenue from operations declined by 5.3% from Q3FY24 to Q3FY25 (YoY), while on a sequential quarter-on-quarter basis, it fell by 6.3% from Q2FY25. From a topline perspective, this seems normal.

However, EBITDA fell by 45% on a YoY basis and 43% on a QoQ basis. This decline in Q3FY25 resulted from a combination of factors - plant idling due to deferred demand, a lag in the recovery of agrochemical intermediates, elevated raw material prices, and oversupply from China, all of which put pressure on the company's margins. Additionally, the dyes and pigments intermediates segment saw reduced margins due to increased feedstock prices. In the phenolics segment, firm input prices and a maintenance shutdown further compressed margins. The cash operating costs (excluding interest) incurred to achieve this level of sales were the highest on both a YoY and QoQ basis, rising to 91.1% of revenue. These factors led to a contraction of EBITDA margins by 631 basis points to just 8.9% in Q3FY25.

Furthermore, due to higher capex and long-term borrowings, depreciation and interest costs jumped by 16% and 109% (YoY), respectively. This impacted PAT, which declined by 51% on a YoY basis and 50% on a QoQ basis. PAT margins stood at just 5.2%, contracting by 490 basis points.

Business Outlook:

Management expects demand to normalize from Q4 onwards following a period of destocking in the agrochemical business and a lag in the recovery of agrochemical intermediates. Additionally, nitric acid and hydrogenation plants are expected to be commissioned by the end of Q4, while MIBK/MIBC and acetophenone plants are slated for completion by H1FY26. The R&D center at Savli, Vadodara, is expected to be completed by March 2025, providing a boost to research activities.

The company is also rapidly expanding its polymer business for long-term growth. It has entered into long-term agreements for the supply of critical feedstock and is acquiring German assets for polycarbonate resins.

These new projects, capacity expansions, cost-improvement measures, and debottlenecking initiatives are expected to enhance the company’s capabilities in the near future.

Easy & quick

Easy & quick

Leave A Comment?