What is the full form of ICICI Bank? – ICICI Full Form

An Overview of ICICI Bank. ICICI acronym stands for Industrial Credit and Investment Corporation of India. It was established in 1955 at the initiative of the World Bank, the Government of India, and representatives of Indian industry. The principal objective was to create a development financial institution for providing project financing to Indian businesses.  In 1999, ICICI Bank became the first Indian bank to be listed on the New York Stock Exchange. In 2014, it became the second-largest investment bank in India. Later in 2014, they also became the third-biggest bank as per market capitalization.

In 1999, ICICI Bank became the first Indian bank to be listed on the New York Stock Exchange. In 2014, it became the second-largest investment bank in India. Later in 2014, they also became the third-biggest bank as per market capitalization.

ICICI Bank's Timeline History:

ICICI Bank's Shareholding Pattern:

| Mar-18 | Mar-19 | Mar-20 | Mar-21 | |

| FIIs | 48.1 | 43.05 | 43.73 | 47.81 |

| DIIs | 41.56 | 45.41 | 44.58 | 41.7 |

| Government | 0.22 | 0.33 | 0.39 | 0.43 |

| Public | 10.12 | 11.21 | 11.31 | 10.06 |

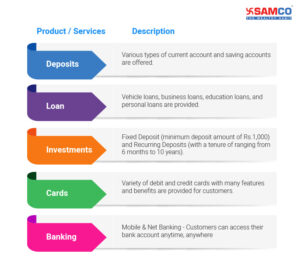

Products and Service Offered by ICICI Bank -

ICICI bank offers the following products and services -  There are various private and public banks operating in India. In this article, let’s compare few private banks with the help of ratios. Ratio analysis gives a broader picture of where a particular company stands in comparison to its competitors.

There are various private and public banks operating in India. In this article, let’s compare few private banks with the help of ratios. Ratio analysis gives a broader picture of where a particular company stands in comparison to its competitors.

ICICI Bank's Important Financial Details:

| Particulars | As of 2020 |

| Revenue | ₹1,49,786.10 crore |

| Operating Income | ₹78,268.2 crore |

| Net Income | ₹9,566.31 crore |

| Net Assets | ₹13,77,292.23 crore |

| Total Equity | ₹1,18,518.45 crore |

Ratio Analysis of ICICI Bank -

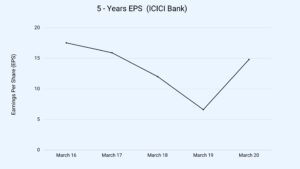

1. Basic Earnings Per Share (EPS) Formula: Basic EPS = (Net Income – Preferred Dividend) /Number of Common Shares Outstanding It indicates how much money a company makes for each outstanding share. Companies with higher EPS are considered to be more profitable. This is readily available in the Income Statement of every listed company. Let's have a look at ICICI Bank's past 5 years EPS trend -

| Years | March 16 | March 17 | March 18 | March 19 | March 20 |

| EPS | 17.53 | 15.91 | 12.02 | 6.61 | 14.81 |

In 2020, we can see an increase in EPS compared to 2019 after a constant decrease since 2016. A constant increase in the EPS figure is considered to be a good sign for the company. The best way to form a better opinion is by comparing the same with its competitors. Comparing ICICI Bank’s Basic EPS with other private banks of India –

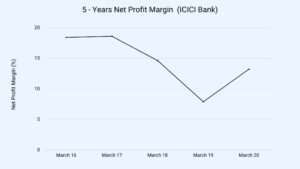

In 2020, we can see an increase in EPS compared to 2019 after a constant decrease since 2016. A constant increase in the EPS figure is considered to be a good sign for the company. The best way to form a better opinion is by comparing the same with its competitors. Comparing ICICI Bank’s Basic EPS with other private banks of India –  We can see that HDFC Bank's EPS is far more than any other private bank in this comparison. Kotak Bank exhibits a constant rise while Axis bank has fluctuating EPS figures. 2. Net Profit Margin Formula: Net Profit margin = Net Profit ⁄ Total revenue x 100 Net profit margin is a strong indicator of a company's success. It measures how much profit is generated as a percentage of sales/revenue. This makes comparison of two or more businesses possible regardless of their size. By tracking the trends in its net profit margin, we can have a picture of the company's operating ability. Here is ICICI bank’s past five years Net Profit margin -

We can see that HDFC Bank's EPS is far more than any other private bank in this comparison. Kotak Bank exhibits a constant rise while Axis bank has fluctuating EPS figures. 2. Net Profit Margin Formula: Net Profit margin = Net Profit ⁄ Total revenue x 100 Net profit margin is a strong indicator of a company's success. It measures how much profit is generated as a percentage of sales/revenue. This makes comparison of two or more businesses possible regardless of their size. By tracking the trends in its net profit margin, we can have a picture of the company's operating ability. Here is ICICI bank’s past five years Net Profit margin -

| Years | March 16 | March 17 | March 18 | March 19 | March 20 |

| NP Margin | 18.42 | 18.60 | 14.63 | 7.90 | 13.23 |

The past five-year net profit margin does not seem very exciting. We can see the net profit margin went up from 7.90% in 2019 to 13.23% in 2020. However, the performance was better in the previous years in 2016 and 2017. We can say that the company is improving its operations and are getter better at managing their expenses. Let’s have a look at how did ICICI Bank’s competitor person during the same period.

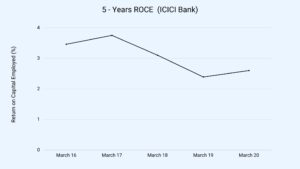

The past five-year net profit margin does not seem very exciting. We can see the net profit margin went up from 7.90% in 2019 to 13.23% in 2020. However, the performance was better in the previous years in 2016 and 2017. We can say that the company is improving its operations and are getter better at managing their expenses. Let’s have a look at how did ICICI Bank’s competitor person during the same period.  Axis Bank has a fluctuating net profit margin. Whereas HDFC Bank and Kotak Bank show a constant increase. It means that they are efficiently converting their sales into profits. 3. Return on Capital Employed (ROCE) Formula: ROCE = Earnings Before Interest and Taxes /Capital Employed This is a long-term profitability ratio that measures how efficiently a company is using its capital. It is used to perform trend analysis for a company. A higher ROCE is always a favorable. It indicates whether a company is using its capital well or not. It is a useful metric to compare profitability across several companies in an industry. Here is ICICI bank’s five-year ROCE trend -

Axis Bank has a fluctuating net profit margin. Whereas HDFC Bank and Kotak Bank show a constant increase. It means that they are efficiently converting their sales into profits. 3. Return on Capital Employed (ROCE) Formula: ROCE = Earnings Before Interest and Taxes /Capital Employed This is a long-term profitability ratio that measures how efficiently a company is using its capital. It is used to perform trend analysis for a company. A higher ROCE is always a favorable. It indicates whether a company is using its capital well or not. It is a useful metric to compare profitability across several companies in an industry. Here is ICICI bank’s five-year ROCE trend -

| Years | March 16 | March 17 | March 18 | March 19 | March 20 |

| ROCE | 3.46 | 3.75 | 3.10 | 2.39 | 2.60 |

We see that the bank isn’t doing better than what it was doing five years back. However, there is a slight increase in 2020’s ROCE compared to 2019. Let’s compare other bank’s performance over the last five-years years to understand who has performed better.

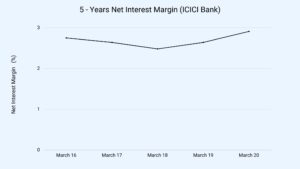

We see that the bank isn’t doing better than what it was doing five years back. However, there is a slight increase in 2020’s ROCE compared to 2019. Let’s compare other bank’s performance over the last five-years years to understand who has performed better.  ICICI bank’s ROCE has reduced over time. While HDFC Bank has generated a consistent ROCE. DCB Bank’s performance is lower than other banks which makes it a less-preferable option for investors. 4. Net Interest Margin Formula: Net Interest Margin = (Interest Returns - Interest Expense) /Average Total Assets Banks provide around 3% interest rate on saving accounts and 6% on fixed deposits. They earn interest on various loans they issue to their clients. For example, car loans, home loans, education loans. The difference between what banks give and what they earn as interest is Net Interest. If it is positive, we can conclude that the bank's operations are profitable. If it is negative, we can say that the bank is not profitable. Here is ICICI Bank’s Net Interest Margin of the past five years –

ICICI bank’s ROCE has reduced over time. While HDFC Bank has generated a consistent ROCE. DCB Bank’s performance is lower than other banks which makes it a less-preferable option for investors. 4. Net Interest Margin Formula: Net Interest Margin = (Interest Returns - Interest Expense) /Average Total Assets Banks provide around 3% interest rate on saving accounts and 6% on fixed deposits. They earn interest on various loans they issue to their clients. For example, car loans, home loans, education loans. The difference between what banks give and what they earn as interest is Net Interest. If it is positive, we can conclude that the bank's operations are profitable. If it is negative, we can say that the bank is not profitable. Here is ICICI Bank’s Net Interest Margin of the past five years –

| Years | March 16 | March 17 | March 18 | March 19 | March 20 |

| NIM | 2.75 | 2.64 | 2.48 | 2.64 | 2.91 |

We can observe a slight improvement in the net margin percentage. The shift shows that the bank is trying to generate more revenue from interest rate differences. Let us compare ICICI bank’s net interest margin with its competitors from the year 2016 to 2020.

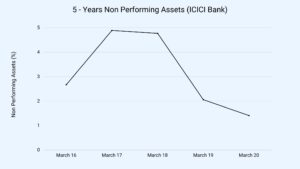

We can observe a slight improvement in the net margin percentage. The shift shows that the bank is trying to generate more revenue from interest rate differences. Let us compare ICICI bank’s net interest margin with its competitors from the year 2016 to 2020.  HDFC Bank and Kotak Bank have the best net interest margins. While ICICI Bank is operating around the 2.5% mark. 5. Non-Performing Assets (NPA) Non-Performing Assets are the ones that cease to generate income for the bank. When the principal or interest payments are not paid by the borrowers, the banks consider them as non-performing assets. Banks often hold a big chunk of NPA. This is because of poor risk management and lending policies. Here is the non-performing asset of ICICI Bank -

HDFC Bank and Kotak Bank have the best net interest margins. While ICICI Bank is operating around the 2.5% mark. 5. Non-Performing Assets (NPA) Non-Performing Assets are the ones that cease to generate income for the bank. When the principal or interest payments are not paid by the borrowers, the banks consider them as non-performing assets. Banks often hold a big chunk of NPA. This is because of poor risk management and lending policies. Here is the non-performing asset of ICICI Bank -

| Years | March 16 | March 17 | March 18 | Mach 19 | March 20 |

| NPA % | 2.67 | 4.89 | 4.77 | 2.06 | 1.41 |

We can observe a sharp and continuous decline in ICICI Bank’s NPA. This is a positive sign indicating that the bank has improved its risk and credit management practices. Let’s have a look at other banks and their NPA level -

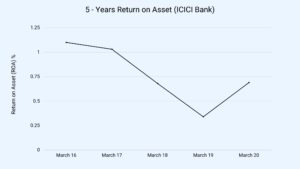

We can observe a sharp and continuous decline in ICICI Bank’s NPA. This is a positive sign indicating that the bank has improved its risk and credit management practices. Let’s have a look at other banks and their NPA level -  There is an overall and continuous decline in NPA levels, which is a good indicator for the sector. However, ICICI Bank’s NPA is still higher than its competitors. HDFC Bank has the lowest NPA while Axis Bank has the highest NPA. 6. Return on Assets Formula: ROA = Net Income / Average Assets

There is an overall and continuous decline in NPA levels, which is a good indicator for the sector. However, ICICI Bank’s NPA is still higher than its competitors. HDFC Bank has the lowest NPA while Axis Bank has the highest NPA. 6. Return on Assets Formula: ROA = Net Income / Average Assets

| Years | March 16 | March 17 | March 18 | March 19 | March 20 |

| ROA | 1.10 | 1.03 | 0.68 | 0.34 | 0.69 |

It measures how efficiently a company can convert the money used to buy an asset into profits. This ratio measures a bank’s ability to generate returns from the deposits it receives. ROA is extremely important while analysing banks. Here is ICICI Bank's five-year ROA trend –  Their return on asset exhibited a constant decline until last year. This does not paint a good picture for the bank. It means that the bank underperformed for years. High NPA could be one reason for low ROA. Let us examine ICICI bank’s five-year ROA and compare them with its competitors -

Their return on asset exhibited a constant decline until last year. This does not paint a good picture for the bank. It means that the bank underperformed for years. High NPA could be one reason for low ROA. Let us examine ICICI bank’s five-year ROA and compare them with its competitors -  HDFC Bank and Kotak Bank have the best ROA. We can observe that ICICI Bank and Axis bank fluctuated on their returns and have underperformed peers by a huge margin

HDFC Bank and Kotak Bank have the best ROA. We can observe that ICICI Bank and Axis bank fluctuated on their returns and have underperformed peers by a huge margin

ICICI Bank’s Subsidiaries:

ICICI Bank's Key Personnel:

Mutual Fund holdings and trends of ICICI Bank Ltd:

| Schemes | Quantity as of March 2021 |

| KOTAK FLEXICAP FUND - GROWTH | 261,945 |

| ICICI PRUDENTIAL BLUECHIP FUND - GROWTH | 231,718 |

| HDFC BALANCE ADVANTAGE FUND - REGULAR PLAN - GROWTH | 199,574 |

| MIRAE ASSET LARGE CAP FUND - REGULAR - GROWTH | 191,069 |

| HDFC FLEXICAP FUND - GROWTH OPTION | 182,537 |

| ICICI PRUDENTIAL BALANCED ADVANTAGE FUND - GROWTH | 178,707 |

| SBI BLUE CHIP FUND - GROWTH | 177,210 |

| ADITYA BIRLA SUN LIFE FRONTLINE EQUITY FUND - GROWTH | 172,488 |

| AXIS BLUECHIP FUND - REGULAR GROWTH | 154,373 |

| HDFC HYBRID EQUITY FUND - REGULAR PLAN - GROWTH | 131,596 |

Visit ICICI's House Group Page and their valuation pages by SAMCO:

Listed stocks:

SAMCO’s Valuation Analysis for ICICI Bank –

You can find such latest valuations easily on Samco’s share price page for every listed company. Take your first step towards stock market trading by opening a FREE Demat account with SAMCO.

You can find such latest valuations easily on Samco’s share price page for every listed company. Take your first step towards stock market trading by opening a FREE Demat account with SAMCO.

Easy & quick

Easy & quick

Leave A Comment?