In this article we cover

- What is NPA?

- Gross NPA and Net NPA

- NPA levels in India – Public sector banks vs Private banks

- Comparing India’s gross NPA with Asian peers

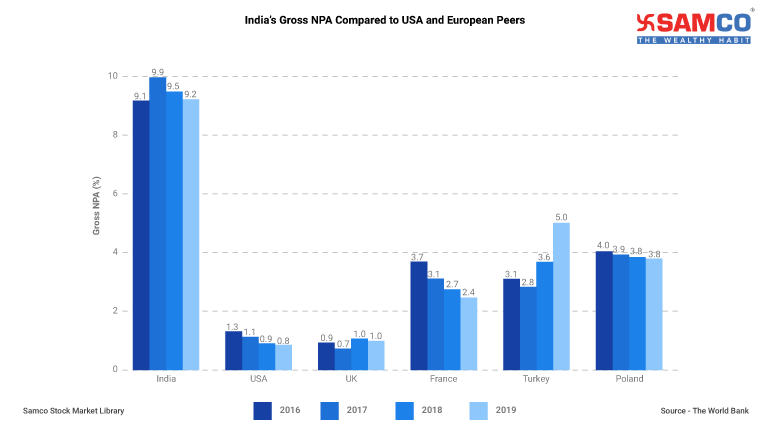

- Comparing India’s gross NPA with European peers

- Implications of pre and post mergers of banks with respect to NPA levels

- Impact of High NPAs and how to interpret it

What is Non-Performing Asset (NPA)?

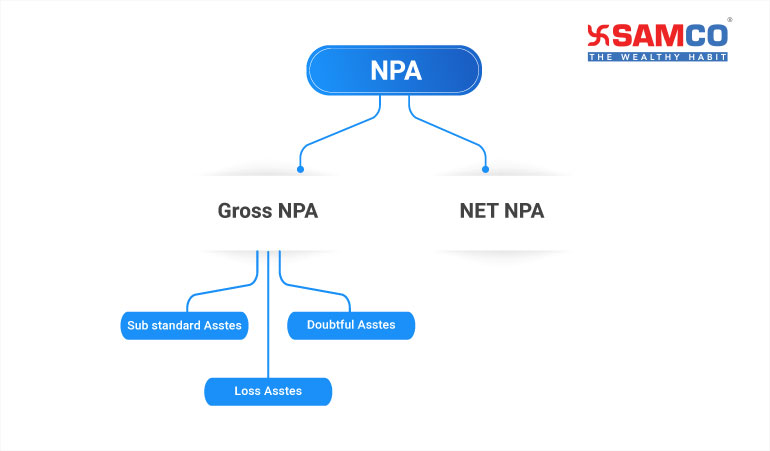

NPA is the most important data which needs to be compared amongst banks. NPAs of a bank can affect other ratios, operations and revenue. Correct analysis of NPA will give you a fair idea of which bank is performing better among its peers. So, straighten up and let’s understand NPA in detail! A bank’s primary source of income is the interest it receives on the loans it provides. When a bank loans money, they expose themselves to credit risk. It means that there are chances that the borrower might fail to repay bank’s loan.. When this happens, the loaned amount is classified as Non-Performing Asset. A loan is classified as a non-performing asset when the repayment is overdue for more than 90 days. It negatively affects bank’s ability to generate adequate income and profitability. A wise manager will always set aside some funds as reserves in case of such bad debts. In banking terms, this is called the Provisional Reserves. Such provisions eat into your profits because you can’t use this money elsewhere. But this is very important for banks to safeguard themselves from huge losses. The total defaults are classified as Gross NPAs (GNPA). The balance amount which remains after deducting the provision is classified as Net NPA (NNPA).Gross NPA and Net NPA

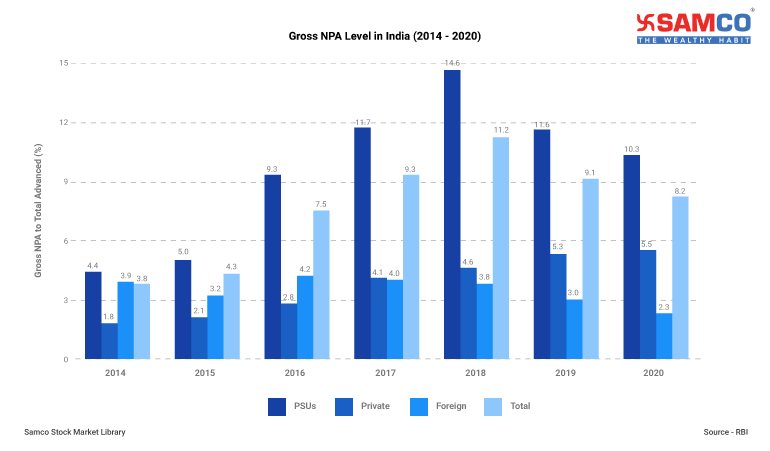

Gross NPA levels in India – Public Sector Banks vs Private banks vs Foreign Banks

Here is the gross NPA comparison between Public Sector Banks (PSUs), Private Banks, and Foreign Banks in India

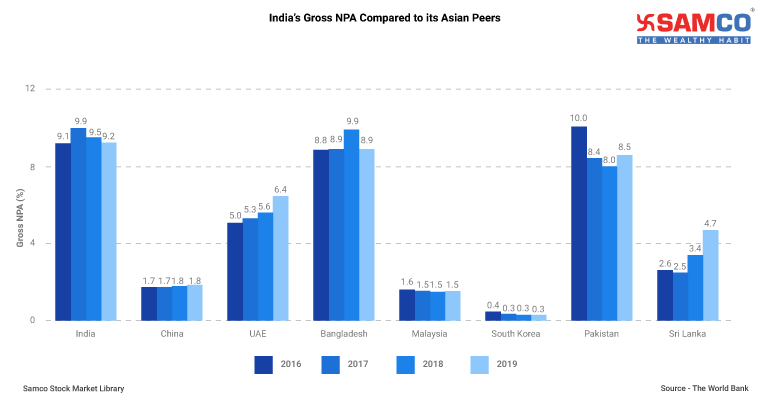

Comparing India’s Gross NPA with Asian Peers:

Implications of pre and post mergers of banks in respect to NPA Level

In 2020, the government announced the amalgamation of 10 PSU banks into four big banks. The merger was effective from April 1, 2020. Oriental Bank of Commerce and United Bank of India were merged into Punjab National Bank. Allahabad Bank into Indian bank, Syndicate Bank into Canara Bank, and Andhra and Corporation Bank into Union Bank of India. Including the past mergers, total number of PSU banks have reduced from 27 to 12. This was a huge step by the government. As an analyst, your duty is to understand how this merger affects the performance the overall banking sector. Mergers results in a bigger capital base and higher liquidity. This reduces government’s burden of recapitalising the public sector banks time and again. Historically, mergers have given great results in terms of saving weak banks. They are crucial for the country’s economy.. Let’s have a look at our recent pre and post-merger data as of March 2020.| Mar-20 | Net NPA Ratio (%) | |

| Pre-Merger | Post-Merger | |

| Punjab National Bank | 5.8 | 5.39 |

| Oriental Bank of Commerce | 5 | |

| United Bank | 4.88 | |

| Canara Bank | 4.18 | 4.08 |

| Syndicate Bank | 4.61 | |

| Union Bank of India | 5.49 | 4.75 |

| Andhra Bank | 4.92 | |

| Corporation Bank | 5.14 | |

| Indian Bank | 3.13 | 3.76 |

| Allahabad Bank | 5.66 | |

| Bank of Baroda | 5.4 | 5.71 |

| Vijaya Bank | 4.1 | |

| Dena Bank | 11.04 |

Impact of High NPAs and how to interpret it

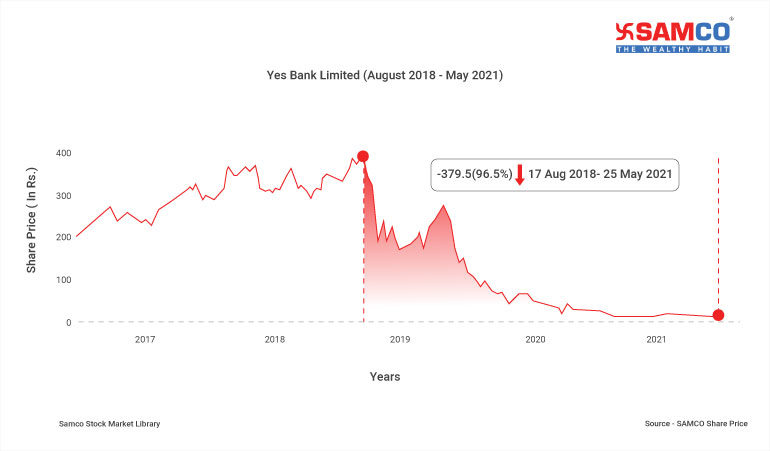

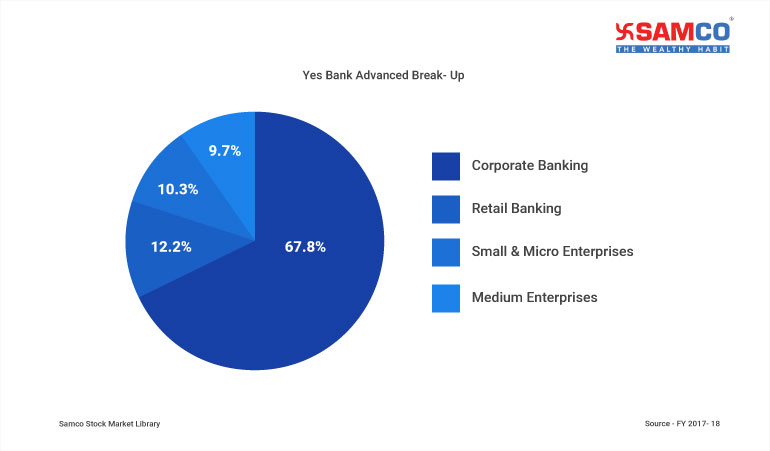

High NPA’s are a red flag for investors. It suggests that the particular bank is not viable. This immediately impacts the banks’ cash flow and future earnings. If these NPAs were paid on time, they would’ve generated additional capital for the banks. This could have been used further by the banks to extend more loans. In fact, banks have to create additional provision if their NPA percentage keeps on increasing. Funds kept aside as provision could have been sourced from the future profits of the bank which otherwise could have been used to maintain stable growth. In simple words, high NPA stops possible future revenue generation.NPA Case Study – Yes Bank’s Rise & Fall

Let’s understand Yes Bank’s scenario. The bank’s stock price fell by almost 90% when the news of its poor financials broke out.

Easy & quick

Easy & quick

Leave A Comment?