In this article, we will discuss

- What Are Strategy Legs?

- What Will Be The Payoff?

- Who Can Deploy This Strategy?

- When Should This Strategy Be Deployed?

- Understanding Strategy Greeks

- Things to Keep In Mind

- Conclusion

Back spread calls are a type of option strategy that involves selling one call option and buying two call options with a higher strike price. This strategy is suitable for traders who are very bullish on the underlying stock or index and expect a large price movement in the near future.

What Are Strategy Legs?

In back spread with calls strategy, you sell one call option and buy two call options such that the strike price of the call option bought is higher than the strike price of the call option sold. Usually, you sell an at-the-money (ATM) call option and buy two out-of-the-money (OTM) call options. For example, if Nifty is trading at 15,000, you can sell one 15,000 call option and buy two 15,500 call options. The ratio of the options is 2:1, meaning you buy twice as many options as you sell.

The reason for choosing this ratio and strike selection is to create a net credit or a zero-cost trade. This means that the premium received from selling the call option is equal to or more than the premium paid for buying the call options. This way, you do not have to pay any upfront cost to enter the trade, and you can benefit from the leverage of the options.

What Will Be The Payoff?

Your maximum profit in this strategy can be unlimited if the underlying stock or index rises significantly above the strike price of the call options bought. Your breakeven in this strategy will depend on whether you have received a net credit or paid a net debit to enter the trade.

If you have a net debit, your breakeven will be:

[Strike price of call option bought + (Difference between strike price of call option sold and call option bought) + Net premium paid]

In this case, you will start making a profit if the underlying stock price starts to move above the breakeven.

For example, if you sell one 15,000 call option for ₹200 and buy two 15,500 call options for ₹100 each, your net debit will be ₹0. Your breakeven will be:

[15,500 + (15,500 - 15,000) + 0] = 16,000

You will make a profit if Nifty closes above 16,000 at expiry.

If you have a net credit, you will have two breakevens. The breakeven on the higher side will be:

[Strike price of call option bought + (Difference between strike price of call option sold and call option bought) - Net premium received]

The breakeven on the lower side will be the strike price of the call option sold plus the net premium received.

In this case, if the underlying stock closes between the two breakevens, you will be in loss. Profits below the lower breakeven will be very less and will be limited to the net credit only. Profits above the upper breakeven can be unlimited.

For example, if you sell one 15,000 call option for ₹300 and buy two 15,500 call options for ₹100 each, your net credit will be ₹100. Your breakevens will be:

[15,500 + (15,500 - 15,000) - 100] = 15,900 (upper breakeven)

[15,000 + 100] = 15,100 (lower breakeven)

You will make a loss if Nifty closes between 15,100 and 15,900 at expiry. You will make a small profit of ₹100 if Nifty closes below 15,100. You will make an unlimited profit if Nifty closes above 16,400.

Who Can Deploy This Strategy?

This strategy can be deployed by veterans who have a moderate risk approach. This strategy can offer good rewards with moderate risk. However, this strategy also requires a high level of accuracy and timing, as the underlying stock or index has to move significantly in the desired direction to make a profit. Therefore, this strategy is not suitable for beginners or conservative traders.

When Should This Strategy Be Deployed?

This strategy should be deployed when you are aggressively bullish on the underlying stock or index and you are confident that there is very little downside risk. However, this strategy should not be used in a sideways or a bearish market, as it can result in losses or low profits.

Understanding Strategy Greeks

The Greeks are the parameters that measure the sensitivity of an option's price to various factors, such as the underlying price, volatility, time, and interest rate. The main Greeks that affect the back spread with calls strategy are delta, gamma, theta, and vega.

- Delta measures the change in the option's price with respect to the change in the underlying price. A positive delta means that the option's price will increase as the underlying price increases, and vice versa. A negative delta means the opposite.

- Gamma measures the change in the delta with respect to the change in the underlying price. A positive gamma means that the delta will increase as the underlying price increases.

- Theta measures the change in the option's price with respect to the change in time. A negative theta means that the option's price will decrease as time passes, and vice versa. A positive theta means the opposite.

- Vega measures the change in the option's price with respect to the change in volatility. A positive vega means that the option's price will increase as volatility increases, and vice versa. A negative vega means the opposite. The back spread with calls strategy has a positive vega, as it benefits from the increase in volatility of the underlying stock or index.

Things To Keep In Mind

The back spread with calls strategy can be a good alternative to the long call strategy. The long call strategy is also deployed when you are aggressively bullish on the underlying stock or index, but it carries a lot of risk in terms of option Greeks. The long call strategy has a high negative theta, which means that the option loses value rapidly as time passes. The back spread with calls strategy, with its unique strike selection, reduces the risk arising from the option Greeks at the cost of shifting the breakeven to a slightly higher level. The back spread with calls strategy has a lower negative theta, which means that the option loses value less rapidly as time passes. The back spread with calls strategy also has a higher positive delta, which means that the option gains value faster as the underlying price increases.

While executing this strategy, it is advisable to execute the buy orders first and then execute the sell orders to get the most out of the margin benefit. This is because buying options requires less margin than selling options, and by buying first, you can reduce the margin requirement for selling later. However, this also exposes you to the risk of price fluctuations between the two transactions, so you should execute them as quickly as possible.

Conclusion

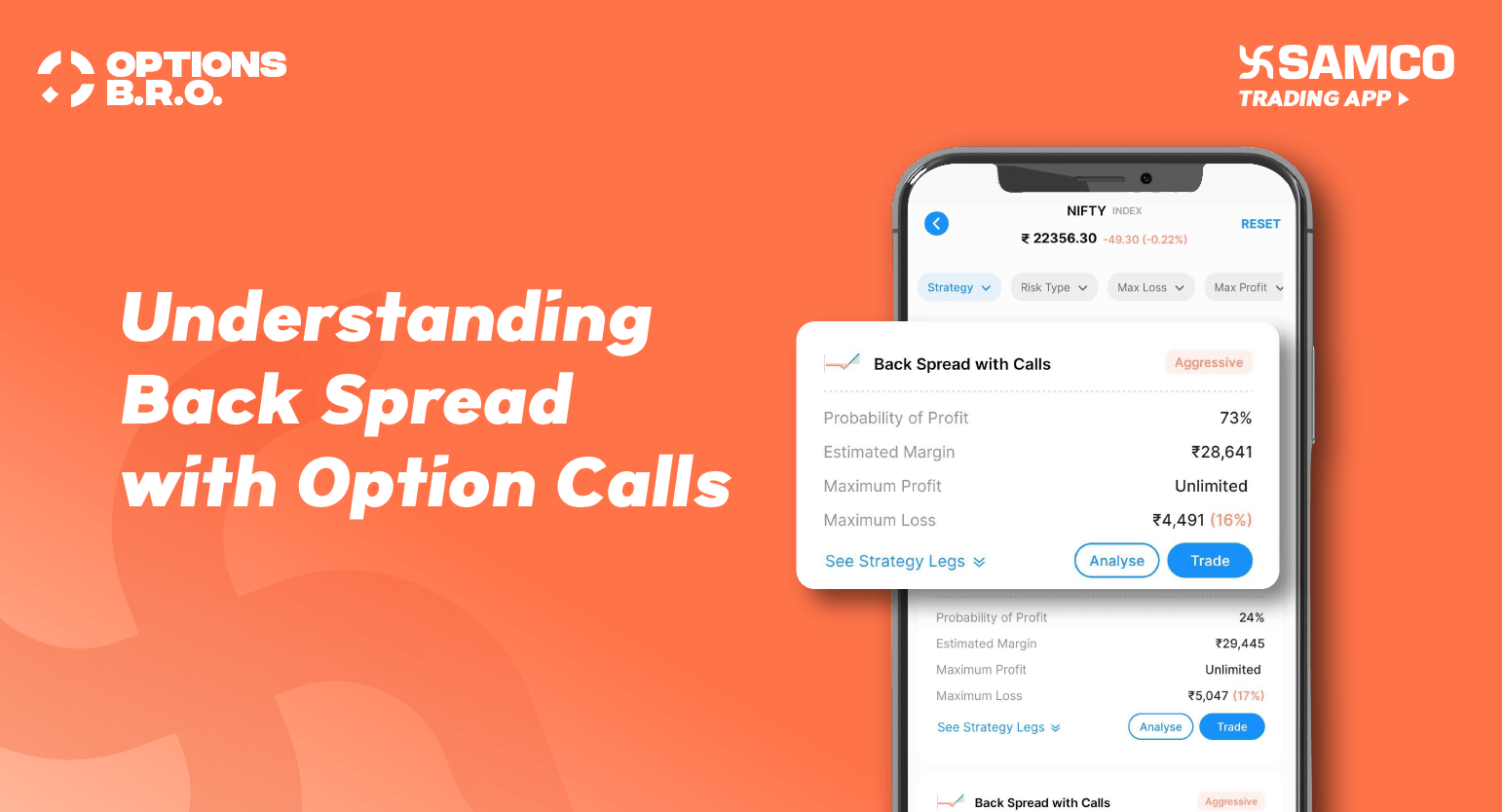

Options B.R.O. is a feature in the Samco trading app that helps you build, research, and optimise your options trading strategies. It uses various parameters, such as implied volatility, option Greeks, and technical indicators, to suggest the best strategies for your market view and risk profile. It also shows you the payoff, breakeven, and Greeks of each strategy, so you can compare and choose the most suitable one.

Disclaimer: INVESTMENT IN SECURITIES MARKET ARE SUBJECT TO MARKET RISKS, READ ALL THE RELATED DOCUMENTS CAREFULLY BEFORE INVESTING. The asset classes and securities quoted in the film are exemplary and are not recommendatory. SAMCO Securities Limited (Formerly known as Samruddhi Stock Brokers Limited): BSE: 935 | NSE: 12135 | MSEI- 31600 | SEBI Reg. No.: INZ000002535 | AMFI Reg. No. 120121 | Depository Participant: CDSL: IN-DP-CDSL-443-2008 CIN No.: U67120MH2004PLC146183 | SAMCO Commodities Limited (Formerly known as Samruddhi Tradecom India Limited) | MCX- 55190 | SEBI Reg. No.: INZ000013932 Registered Address: Samco Securities Limited, 1004 - A, 10th Floor, Naman Midtown - A Wing, Senapati Bapat Marg, Prabhadevi, Mumbai - 400 013, Maharashtra, India. For any complaints Email - grievances@samco.in Research Analysts -SEBI Reg.No.-INHO0O0005847.

Easy & quick

Easy & quick

Leave A Comment?