Background:

NATCO Pharma Limited (NATCO) is a vertically integrated, research and development focused pharmaceutical company engaged in developing, manufacturing, and marketing complex products for niche therapeutic areas.

It has established its presence in all three business segments viz. finished dosage formulations (“FDF”), active pharmaceutical ingredients (“APIs”), and Contract Manufacturing Business.

Present:

Today it announced its Dec-24 quarter ending results and the share price tumbled by more than 18% in a single day.

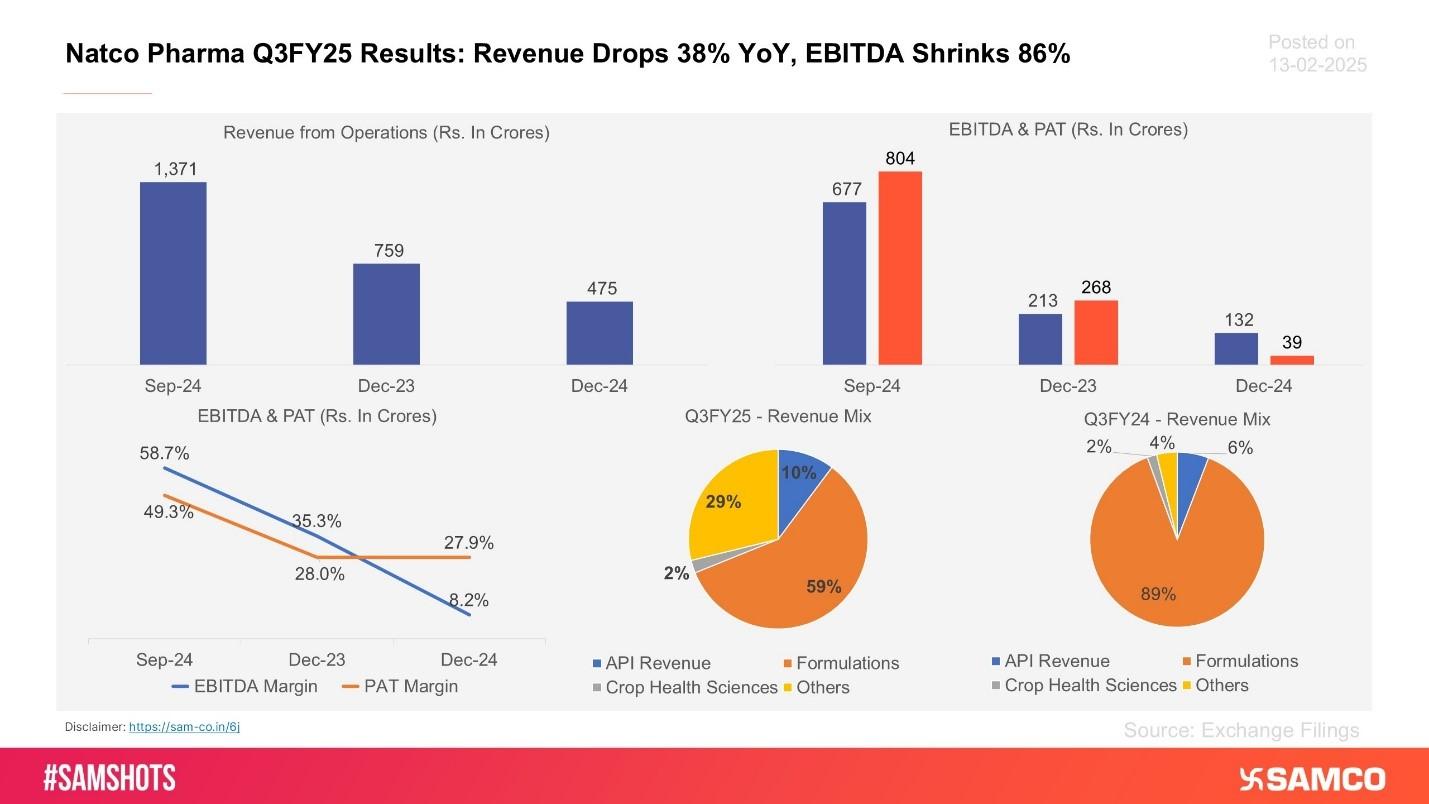

This decline was primarily driven by lower export formulation sales, which dropped from ₹605 crore in Dec-23 to ₹286 crore in Dec-24, marking a 53% reduction. Its main revenue driver being Revlimid sales dropped significantly impacting the entire financials.

Further, the consolidated revenue from operations declined by 38% year-on-year (YoY) from Dec-23 to Dec-24 and fell by 65% sequentially on a quarter-on-quarter (QoQ) basis.

This significant drop in topline impacted the cost structure, as Selling, General & Administrative (SG&A) expenses, which accounted for 43% of revenue in Dec-23, surged to 74% in Dec-24. While the absolute expense figures may not fully capture the impact, the increase as a percentage of revenue highlights the material effect on profitability.

EBITDA declined by 86% YoY and 95% QoQ, with EBITDA margins shrinking to just 8.2%, a steep contraction of 27.2 percentage points from Dec-23.

The company managed to report a positive PAT primarily due to other income component of ₹176 crore. However, the bottom line declined by 38% YoY and 80% QoQ. Despite the earnings drop, PAT margins remained steady at 28%.

What Next:

With several Para IV molecules awaiting approval, including 13 already approved, the management remains confident that its two formulations of Semaglutide, along with upcoming product launches in the coming months, will help restore revenue growth.

Easy & quick

Easy & quick

Leave A Comment?