Introduction: Wish to master fundamental analysis?

Then learning to interpret the cash flow (CF) statement is amongst its most critical elements. The statement of cash flows is one of the main financial statements, alongside the balance sheet, income statement and statement of stockholders' equity. As the income statement is prepared under the accrual basis of accounting the revenues and expenses reported may not have been collected or paid for yet. While these facts can be uncovered by reviewing the balance sheet, all this information has already been integrated into the cash flow statement. As a result, savvy investors utilize this important financial statement. Following are smart pointers as to how to interpret a statement of cash flows. Latest annual report of Infosys here used as a references.

What is Cash Flow Statement?

The cash flow statement reports the cash received and used during a specific period of time - say a quarter or a given financial year as specified in the heading. [caption id="attachment_2603" align="aligncenter" width="660"] Cash Flow Statement for a period under consideration[/caption]

Many investors believe in the mantra “cash is the king. Markets value companies that consistently generate more cash than they use. Such a company will be able to increase shareholder value by paying higher dividends, buying back some of its stock, reducing debt or acquiring another company. Many companies try to woo investors by showcasing a high EBITDA (earnings before interest, taxes, depreciation and amortization). Smart investors understand that this is an accounting invention that should not be looked at while valuing a company. Interest and taxes are real cash expenses that are hidden away when EBITDA is used as a measure of performance. Bad loans and any changes to working capital accounts (accounts receivable and inventory) are worryingly not captured in EBITDA.

The cash flow statement organizes this information into four categories, namely:

Cash Flow Statement for a period under consideration[/caption]

Many investors believe in the mantra “cash is the king. Markets value companies that consistently generate more cash than they use. Such a company will be able to increase shareholder value by paying higher dividends, buying back some of its stock, reducing debt or acquiring another company. Many companies try to woo investors by showcasing a high EBITDA (earnings before interest, taxes, depreciation and amortization). Smart investors understand that this is an accounting invention that should not be looked at while valuing a company. Interest and taxes are real cash expenses that are hidden away when EBITDA is used as a measure of performance. Bad loans and any changes to working capital accounts (accounts receivable and inventory) are worryingly not captured in EBITDA.

The cash flow statement organizes this information into four categories, namely:

- Operating activities

- Investing activities

- Financing activities

- Supplemental information

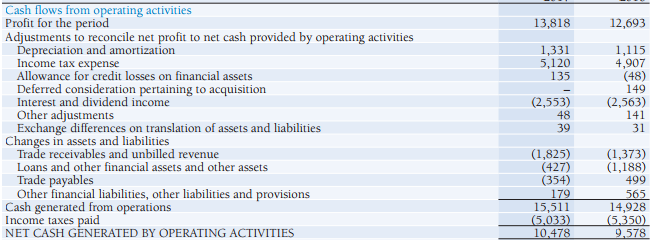

Cash Flows From Operating Activities:

[caption id="attachment_2604" align="aligncenter" width="652"] Cash Flow from Operating Activities - Cash Flow Statement[/caption]

This section starts with net income of the company and converts it from the accrual basis to the cash basis. This is done by using the changes in the balances of current assets and current liabilities during the same period. This could include accounts receivables, inventory, supplies, prepaid Insurance, notes payable, accounts payable, wages payable, payroll taxes payable, interest payable, income taxes payable, unearned revenues, trade debtors, trade creditors, other current assets and liabilities. As some of the revenues and expenses recorded in income statement are non-cash; adjustments are also made for depreciation and gains or losses from long-term assets.

Cash Flow from Operating Activities - Cash Flow Statement[/caption]

This section starts with net income of the company and converts it from the accrual basis to the cash basis. This is done by using the changes in the balances of current assets and current liabilities during the same period. This could include accounts receivables, inventory, supplies, prepaid Insurance, notes payable, accounts payable, wages payable, payroll taxes payable, interest payable, income taxes payable, unearned revenues, trade debtors, trade creditors, other current assets and liabilities. As some of the revenues and expenses recorded in income statement are non-cash; adjustments are also made for depreciation and gains or losses from long-term assets.

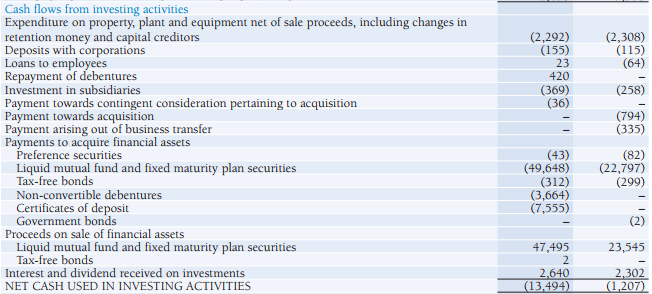

Cash Flows from Investing Activities:

[caption id="attachment_2605" align="aligncenter" width="652"] Cash Flow from Investing Activities - Cash Flow Statement[/caption]

This section captures the purchase and sales of long-term investments, property, plant and equipment. In other words, it reports any changes in the long-term assets account. This could include long-term investments, land, buildings, equipment, furniture & fixtures and vehicles.

Cash Flow from Investing Activities - Cash Flow Statement[/caption]

This section captures the purchase and sales of long-term investments, property, plant and equipment. In other words, it reports any changes in the long-term assets account. This could include long-term investments, land, buildings, equipment, furniture & fixtures and vehicles.

Cash Flows from Financing Activities:

[caption id="attachment_2606" align="aligncenter" width="645"] Cash Flow from Financing Activities - Cash Flow Statement[/caption]

The changes in the balances of the long-term liability and stockholders’ equity for the same period. These could include notes payable (due after one year), bonds payable, deferred Income taxes, preferred stock, common stock, retained earnings and treasury stock.

Cash Flow from Financing Activities - Cash Flow Statement[/caption]

The changes in the balances of the long-term liability and stockholders’ equity for the same period. These could include notes payable (due after one year), bonds payable, deferred Income taxes, preferred stock, common stock, retained earnings and treasury stock.

Supplemental information:

[caption id="attachment_2607" align="aligncenter" width="648"]Red Flags:

- Net profit not converted to cash:

- Bad asset creation:

- Capitalizing operating expenses: Companies sometimes move items from operating expenses to balance sheet as an asset and depreciate (or amortize) it over years. This boosts operating cash flow as some of the expenses are shifted to investing activities. An investor should be alert for any spikes in capital expenses that are accompanied by a proportionate increase in cash from operating activities, and inspect it further to be sure that no fishy business is going on.

- Classifying inventory as investments: Typically, the monies spent on acquiring or producing inventories that will be sold to the customer should be part of operating cash flow (outflow). But sometimes these are reported in cash flows from investing activities and amortized over one year. This treatment translates into a big boost to operating cash flow. Investors need to take a judgment call on such misclassification and it is important to question any large investment outflow that other players in the industry normally classify as cost of operations.

Easy & quick

Easy & quick

Leave A Comment?